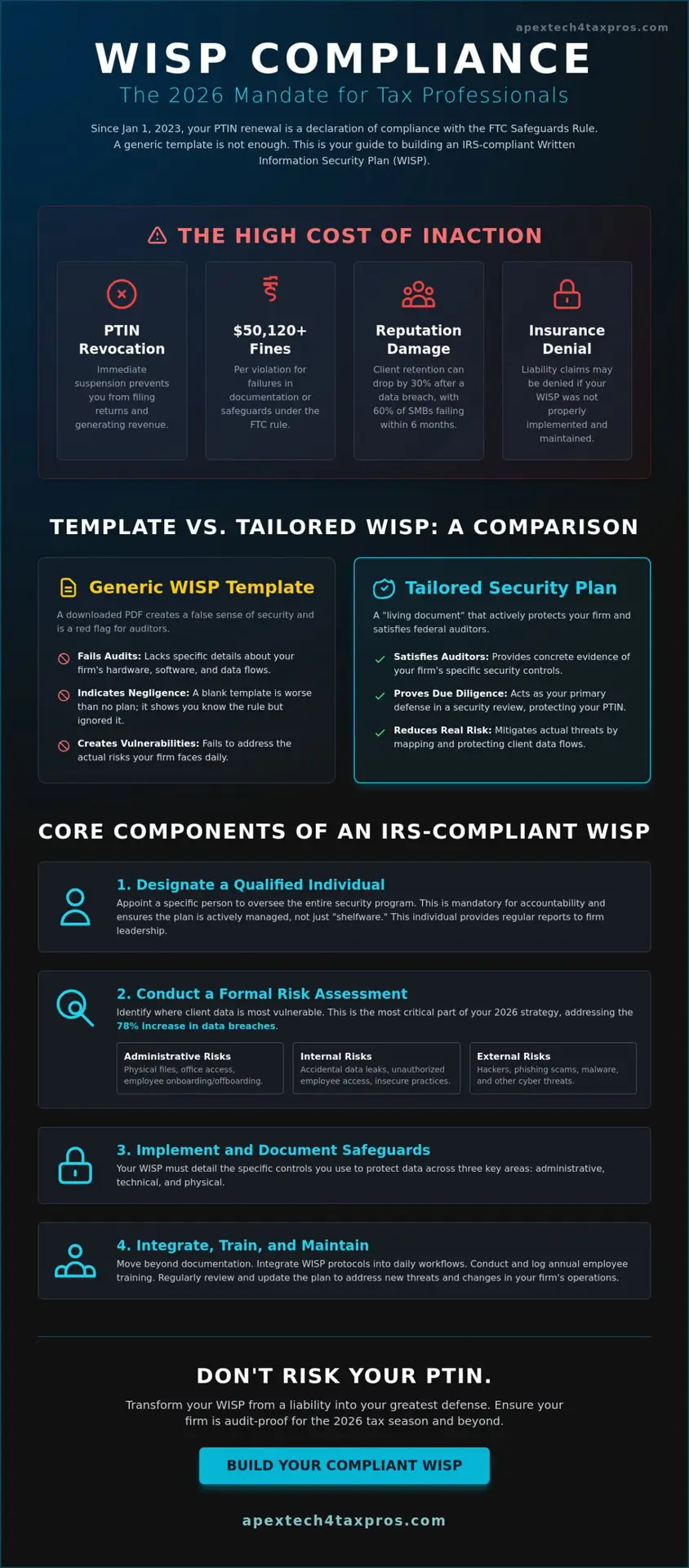

Your PTIN renewal is no longer a simple administrative task; it’s a formal declaration that your firm maintains a comprehensive security plan under the Gramm-Leach-Bliley Act. Since January 1, 2023, the IRS has required tax professionals to check a specific box confirming they have a Written Information Security Plan in place. Failing to produce this document during a random audit can lead to immediate PTIN revocation or significant federal penalties. You likely recognize that a generic wisp template for accountants is a necessary starting point, but it isn’t a “set it and forget it” solution for the 2026 tax season.

We agree that the technical jargon in IRS Publication 4557 can feel overwhelming when you’re focused on high-stakes tax preparation. This article promises to help you bridge the gap between regulatory requirements and your firm’s daily operations. We’ll show you how to transform a static template into a tailored security framework that satisfies federal auditors. We’ll examine the specific internal risks you must document, the 2026 compliance standards, and the exact steps to secure your client’s most sensitive data with confidence.

Key Takeaways

- Navigate the legal intersection of the FTC Safeguards Rule and IRS mandates to ensure your firm meets every 2026 regulatory standard.

- Identify the core pillars of an IRS-compliant plan, including the designation of a Responsible Official and the execution of a formal risk assessment.

- Learn how to transform a generic wisp template for accountants into a tailored security framework that bridges the gap between IT requirements and tax law.

- Master the step-by-step process for inventorying hardware and mapping sensitive client data flows from initial intake to final archival.

- Discover how to move beyond documentation by integrating WISP protocols into your daily tax preparation workflows to foster a firm-wide culture of data integrity.

Understanding the WISP Mandate: Why Accountants Need More Than a PDF

The IRS Publication 5708 defines the Written Information Security Plan (WISP) as a living document that details the administrative, technical, and physical safeguards used to protect taxpayer information. This requirement isn’t a suggestion; it’s a federal mandate that carries the weight of law. Since the FTC updated the Safeguards Rule in December 2021, the legal burden on tax professionals has intensified. Every PTIN holder, whether a solo practitioner or a partner in a large firm, must maintain a WISP to remain compliant in 2026. A generic wisp template for accountants often fails because it lacks the tailored technical controls required by the modern IRS regulatory environment.

A WISP serves as more than a simple security policy. It’s a comprehensive framework that bridges the gap between tax preparation and IT security. Many professionals fall into the “False Sense of Security” trap by downloading a free PDF and filing it away without customization. During an IRS audit, this approach usually backfires. Auditors look for evidence that the plan is active and reflects the firm’s actual hardware and software environment. A blank template can be more dangerous than no plan, as it indicates a failure to perform the required risk assessments and documented safeguards.

The Evolution of IRS Security Requirements

Federal oversight for tax professionals has transformed significantly over the last decade. The journey began with IRS Publication 4557, which established baseline safeguarding principles for the industry. By 2023, the IRS integrated more rigorous documentation requirements under the Gramm-Leach-Bliley Act to address rising cyber threats. The 2026 standards now demand specific incident response protocols and annual employee training logs to ensure data integrity. A WISP is a mandatory blueprint for data protection.

Consequences of Non-Compliance

The risks of ignoring these mandates are substantial and measurable. The IRS has the authority to suspend PTINs for failing to provide a WISP during a security review or after a breach. Additionally, civil penalties for FTC Safeguards Rule violations can exceed $50,120 per violation. Beyond federal fines, the damage to a firm’s reputation is often permanent. Industry data shows that 60% of small businesses fail within six months of a significant data breach. Your WISP acts as your primary defense, proving to regulators that you took reasonable steps to secure sensitive client data.

- PTIN suspension prevents you from filing returns and generating revenue.

- Federal fines can reach $50,120 per occurrence for documentation failures.

- Client retention drops by an average of 30% after a reported data breach.

- Professional liability insurance may deny claims if a WISP wasn’t properly maintained.

Relying on a generic wisp template for accountants without professional guidance leaves your firm vulnerable. Compliance requires a disciplined, vigilant approach to data security that goes beyond checking a box. As your trusted advisor, we focus on ensuring your documentation meets the clinical precision required by federal regulators while protecting your clients’ most sensitive information.

Core Components of an IRS-Compliant WISP in 2026

A compliant wisp template for accountants must begin with the designation of a “Qualified Individual.” This isn’t just a clerical role. Both the IRS and the FTC Safeguards Rule require a specific person to oversee the entire security program. Accountability prevents the plan from becoming “shelfware” that gathers dust until an audit occurs. This official is responsible for coordinating the security program and providing regular reports to your firm’s leadership.

Your risk assessment framework needs to evaluate three specific areas to be effective. Administrative risks involve how you handle physical files and office access. Internal risks focus on employee behavior or accidental data leaks. External risks address hackers, phishing, and malware. A 2023 report from the Identity Theft Resource Center noted a 78% increase in data breaches, making this assessment the most critical part of your 2026 strategy. It’s about identifying where your data is most vulnerable and applying logic to its protection.

Information systems safeguards have evolved. Moving beyond simple passwords is non-negotiable. Your plan must detail the implementation of multi-factor authentication (MFA) for all systems containing taxpayer information. Encryption should be applied to data at rest and in transit. These technical controls act as the digital locks on your firm’s most sensitive assets.

Detection and response protocols are your emergency playbook. If a breach occurs, your WISP must define how you’ll identify the incident and the timeline for notifying the IRS Stakeholder Liaison. It’s better to have a plan you never use than to scramble during a crisis.

Employee Management and Training Mandates

You can’t protect data if your team doesn’t understand the stakes. Every wisp template for accountants should include a section for documenting background checks and signed confidentiality agreements for every new hire. IRS Publication 4557 emphasizes that cybersecurity awareness training isn’t a one-time event. You’ll need to record completion dates for every staff member to satisfy auditors. These records prove you’ve fostered a culture of vigilance and personal accountability within your firm.

External Risk Management: Third-Party Service Providers

Your security is only as strong as your weakest vendor. Whether it’s your cloud storage provider or tax prep software, you must vet their security protocols before signing a contract. Your WISP should require specific language in vendor agreements that mandates their compliance with federal standards. We recommend performing annual vendor risk reviews to ensure their safeguards haven’t lapsed over time. If you feel overwhelmed by these technical requirements, partnering with a specialized IT advisor can help bridge the gap between tax law and digital security.

WISP Templates vs. Customized Security Plans: A Practical Comparison

Choosing a wisp template for accountants often seems like the fastest path to checking a regulatory box. These “DIY” templates are typically low cost or even free, but they demand a high level of manual effort from the firm owner. A common pitfall involves “copy-paste” errors where a firm accidentally commits to security protocols they don’t actually have the infrastructure to support. This creates a “compliance gap” that becomes a major liability during an IRS audit or a data breach investigation. If your document claims you use encrypted drives but your staff saves files to unencrypted USB sticks, your WISP is essentially a roadmap of your own negligence.

A professional WISP represents a higher initial investment, yet it provides a “Dual-Expert” bridge between technical IT requirements and federal tax law. While a template is a static document, a professional plan is a living framework. It addresses the specific accounting workflows that generic documents miss, such as the secure transmission of sensitive K-1s or the management of multi-factor authentication across various tax software platforms. Scalability is another critical factor. As your firm grows, perhaps adding five remote staff members by 2026, your security plan must evolve to cover new endpoints and home-office vulnerabilities. A static template won’t grow with you; it will only hold you back.

When a Free Template is Enough (and When It Is Not)

A basic wisp template for accountants might suffice for a solo practitioner with a minimal client base and no employees. However, as technical complexity increases, the risk of using outdated templates grows. Many free resources found on non-specialized websites haven’t been updated to reflect the critical 2023 changes to the FTC Safeguards Rule. The IRS explicitly cautions tax professionals against using “canned” or boilerplate security plans. According to the IRS guidance on WISP, your plan must be appropriate to the size and complexity of your firm. A generic document that doesn’t reflect your actual data volume and hardware inventory fails to meet this legal standard.

The Value of a Tailored Security Assessment

A professional risk assessment is the prerequisite for a valid WISP. It identifies the specific vulnerabilities within your firm’s unique tech stack. This process informs the customization of your plan, ensuring that your IT security protocols don’t hinder your tax preparation efficiency. We focus on bridging the gap between high-level cybersecurity and the daily realities of a busy tax office. Learn more about our customized WISP solutions to see how a tailored approach protects your practice. By aligning your administrative, technical, and physical safeguards with your actual business practices, you move from a state of vulnerability to one of secure, documented compliance.

How to Customize Your WISP Template: A Step-by-Step Guide

A generic wisp template for accountants provides the skeleton, but your firm’s specific operations provide the muscle. To achieve 2026 compliance, you must move beyond templates and document your actual environment. Compliance isn’t a “set and forget” task; it’s a living protocol that reflects your daily workflows and security culture.

Step 1 involves a granular hardware registry. This list must include every desktop, laptop, and server, but it also needs to account for mobile devices and home office equipment used by remote staff. According to 2023 industry surveys, 43% of data leaks in small firms stem from unmanaged personal devices. You must also identify “Shadow IT,” which includes unauthorized file-sharing apps or personal email accounts used for firm business. To satisfy IRS auditors, you should explicitly document that sensitive client data is protected by AES-256 bit encryption at rest and TLS 1.2 or higher during transit.

Step 2 and 3 require mapping data flow and defining access. Trace a tax return from the initial client intake through the filing process and into long-term archival. Access controls ensure that a seasonal intern doesn’t have the same administrative privileges as a senior partner. This principle of least privilege reduces your internal risk surface significantly.

Inventory and Data Mapping

Effective data mapping identifies every touchpoint where a Social Security Number or bank detail exists. Your registry should catalog serial numbers and physical locations for all hardware. Documenting encryption protocols is vital; you must verify that your cloud storage and local backups utilize industry-standard encryption to prevent unauthorized access during a physical theft or digital intercept. Don’t ignore physical security like locking file cabinets or clean-desk policies.

Drafting the Incident Response Plan

Your WISP must distinguish between a security event and a data breach. A security event might be a failed brute-force login attempt, while a breach involves the actual compromise of PII. Your Incident Response Plan (IRP) acts as your firm’s emergency playbook. It needs to be actionable and tailored to your specific staff size.

When a breach occurs, time is your enemy. Your IRP should list exact communication protocols, starting with your local IRS Stakeholder Liaison and state tax agencies. You’ll also need to notify local law enforcement and affected clients as required by state “notice of loss” laws. Don’t let your IRP sit on a shelf. Conduct a “tabletop exercise” annually. This simulated drill tests your team’s readiness and ensures your response is reflexive rather than panicked.

Step 5 is the commitment to maintenance. Establish a recurring calendar invitation for an annual plan review. This ensures your wisp template for accountants evolves alongside new IRS mandates and emerging cyber threats. Regular updates turn a static document into a robust shield for your practice.

Ready to secure your firm’s future? Download our professional WISP assessment checklist to bridge the gap between IT and compliance.

Implementing Your WISP: From Documentation to Firm Culture

Signing your security document is merely the start of a long compliance journey. A static file sitting in a digital folder won’t stop a data breach. You’ve got to weave these protocols into the actual fabric of your daily tax preparation workflows. This means every staff member needs to understand how to handle sensitive PII from the moment a client shares their first document. Effective implementation involves integrating your wisp template for accountants into your standard operating procedures. It’s about making security second nature rather than a seasonal afterthought.

Data integrity and availability are central to the 2026 IRS requirements. You must implement secure cloud backup systems that do more than just store files. These systems need to provide a verifiable audit trail and off-site redundancy. If a hardware failure or a ransomware attack occurs, your firm must be able to restore operations quickly without losing a single taxpayer record. This level of readiness is what separates compliant firms from those at risk of heavy federal penalties and reputational ruin.

Fostering a Culture of Security

Compliance fatigue is a real threat to accounting firms. Staff members often see new security rules as hurdles that slow down their work during the busy season. To overcome this, leadership buy-in is non-negotiable. When partners and senior managers consistently follow the WISP protocols, the rest of the team views data protection as a core value rather than a chore. You can also leverage your security posture as a significant marketing asset. Highlighting your rigorous data safeguards builds immediate trust with clients who are increasingly worried about identity theft. Showing them a formalized security plan can distinguish your practice from competitors who only do the bare minimum.

The Apex Advantage: Bridging the Gap

Apex Tech 4 Tax Pros serves as your Dual-Expert Guardian in an environment where threats change weekly. We bring 20 years of specialized experience in both the tax industry and high-stakes IT security. This dual perspective allows us to provide a wisp template for accountants that isn’t just a generic document but a practical roadmap tailored to your specific needs. We ensure your plan evolves alongside IRS Publication 5708 and other regulatory shifts. We’ve spent decades bridging the gap between technical requirements and the reality of running a busy tax office. Our mission is to protect your reputation while you focus on serving your clients.

Take the next step in securing your firm’s future: Download our Free WISP Template or Schedule a Consultation.

Securing Your Firm’s Regulatory Future Beyond 2026

Adopting a static wisp template for accountants isn’t enough to satisfy the evolving standards of IRS Pub 5708 or the FTC Safeguards Rule. As we approach the 2026 filing season; your documentation must transition from a dormant file into a living component of your firm’s daily operations. Successful compliance requires bridging the gap between technical IT requirements and the practical workflows of a busy tax practice. You’ve learned that a customized plan protects your data integrity while ensuring every team member understands their role in safeguarding sensitive taxpayer information.

Apex Tech 4 Tax Pros brings 20+ years of experience to this specialized intersection of tax law and cybersecurity. As a family-owned boutique firm with national reach; we provide the professional authority you need to navigate these high-stakes regulatory burdens. We’ll help you move past generic templates to implement a strategy that’s specifically engineered for your unique business structure. Protect your firm with a customized WISP from Apex Tech 4 Tax Pros. You’ve worked hard to build your practice; so let’s ensure it stays protected and compliant for years to come.

Frequently Asked Questions

Is a WISP really mandatory for a solo CPA or a one-person tax office?

Yes, federal law requires every tax professional to maintain a Written Information Security Plan regardless of their firm’s size. The Gramm-Leach-Bliley Act mandates that even solo practitioners with zero employees must implement these safeguards. When you renew your PTIN annually, you’re required to check a box confirming you have a WISP in place. Failing to maintain this document can lead to increased IRS oversight or civil penalties under the FTC Safeguards Rule.

What is the difference between IRS Publication 4557 and Publication 5708?

IRS Publication 4557 outlines the broad security standards for protecting taxpayer data, while Publication 5708 serves as the specific guide for creating a WISP. Think of Publication 4557 as the regulatory “what” that defines the seven key areas of security every firm must address. In contrast, Publication 5708 is a 28-page document released in 2022 that provides the actual framework and template for your written plan. Both are essential for maintaining 2026 compliance standards.

How often do I need to update my Written Information Security Plan?

You must update your security plan at least once every 12 months or whenever a change occurs in your firm’s technical infrastructure. If you adopt new tax software or move to a cloud-based server in 2026, your document must reflect those specific modifications immediately. Regular annual reviews ensure your security protocols align with the latest IRS requirements and evolving cyber threats. Our 20 years of experience shows that static documents quickly become obsolete and non-compliant.

Can I use a generic WISP template for my accounting firm?

You shouldn’t rely on a generic wisp template for accountants without customizing it to reflect your firm’s unique hardware, software, and data flow. A one-size-fits-all document often fails to meet the “reasonable and appropriate” standard set by the FTC. Auditors quickly identify firms that haven’t tailored their administrative, technical, and physical safeguards to their actual daily operations. To ensure data integrity, your plan must detail the specific vendors and encryption methods you use every day.

What should I do if my firm experiences a data breach but I have a WISP in place?

You should immediately execute the incident response protocol outlined in your WISP to mitigate further data loss. This involves notifying the IRS Stakeholder Liaison within 24 hours of discovery and alerting all affected clients as required by state laws. Having a documented plan demonstrates to regulators that you took proactive steps to protect data. This professional preparation can significantly reduce potential fines or legal liability following a security event.

Does a WISP cover remote employees and home office setups?

Your WISP must explicitly cover 100 percent of the locations where taxpayer data is accessed, including home offices and remote work environments. The FTC Safeguards Rule requires that your security measures extend to any device or network used for business purposes. This means your plan should detail the encryption standards, multi-factor authentication, and physical security protocols used by your staff. Bridging the gap between office and home security is a core requirement for 2026 compliance.

What are the most common mistakes accountants make when filling out a WISP template?

The most frequent mistake is failing to designate a specific Security Coordinator responsible for overseeing the plan’s implementation. Many firms also leave their wisp template for accountants incomplete by failing to list every third-party service provider that handles client data. Without naming your specific cloud storage providers and software vendors, your plan lacks the technical precision required for federal audits. A vague plan is often treated as no plan at all by regulatory bodies.

How does the FTC Safeguards Rule impact my WISP requirements in 2026?

The FTC Safeguards Rule requires non-banking financial institutions, including tax preparers, to implement specific technical safeguards like data encryption and multi-factor authentication by 2026. This rule mandates that firms with 5,000 or more consumer records must report any security event involving at least 500 people to the FTC within 30 days. It transitions firms from simple document storage to active, monitored cybersecurity management. These standards ensure that sensitive data remains under constant, disciplined protection.