Your Written Information Security Plan is not a static document you file away; it is a living framework that fails the moment it stops reflecting your firm’s actual daily behaviors. You’ve likely felt the mounting pressure of the 2026 filing season, especially with the IRS requiring updated plans that reflect the latest Publication 5708 changes. It’s understandable to feel overwhelmed by technical jargon while managing a heavy client load. Identifying common wisp mistakes for accountants is the first step toward securing your practice against FTC Safeguards Rule penalties that can now reach $50,120 per violation.

We recognize the weight of these regulatory burdens and the genuine concern that a single oversight could lead to a data breach. Our mission is to provide the protective reassurance required to move your firm from a state of vulnerability to secure compliance. This article identifies the most frequent documentation errors, addresses new 2026 privacy requirements in states like Indiana and Kentucky, and provides a clear roadmap to ensure your sensitive client data remains in safe, capable hands.

Key Takeaways

- Understand the mandatory nature of a Written Information Security Plan for any firm holding a PTIN under IRS Publication 4557.

- Identify common wisp mistakes for accountants, such as the “template trap” where generic documents fail to reflect a firm’s actual daily operations.

- Learn how to bridge the compliance gap by integrating documented cybersecurity awareness training to address the human element of data security.

- Discover the risks associated with “shadow IT” and how to align your administrative access levels with the Principle of Least Privilege.

- Establish a methodical process for auditing your IT assets to ensure your security framework meets rigorous 2026 regulatory standards.

What is a WISP and Why Do Most Accounting Firms Get It Wrong?

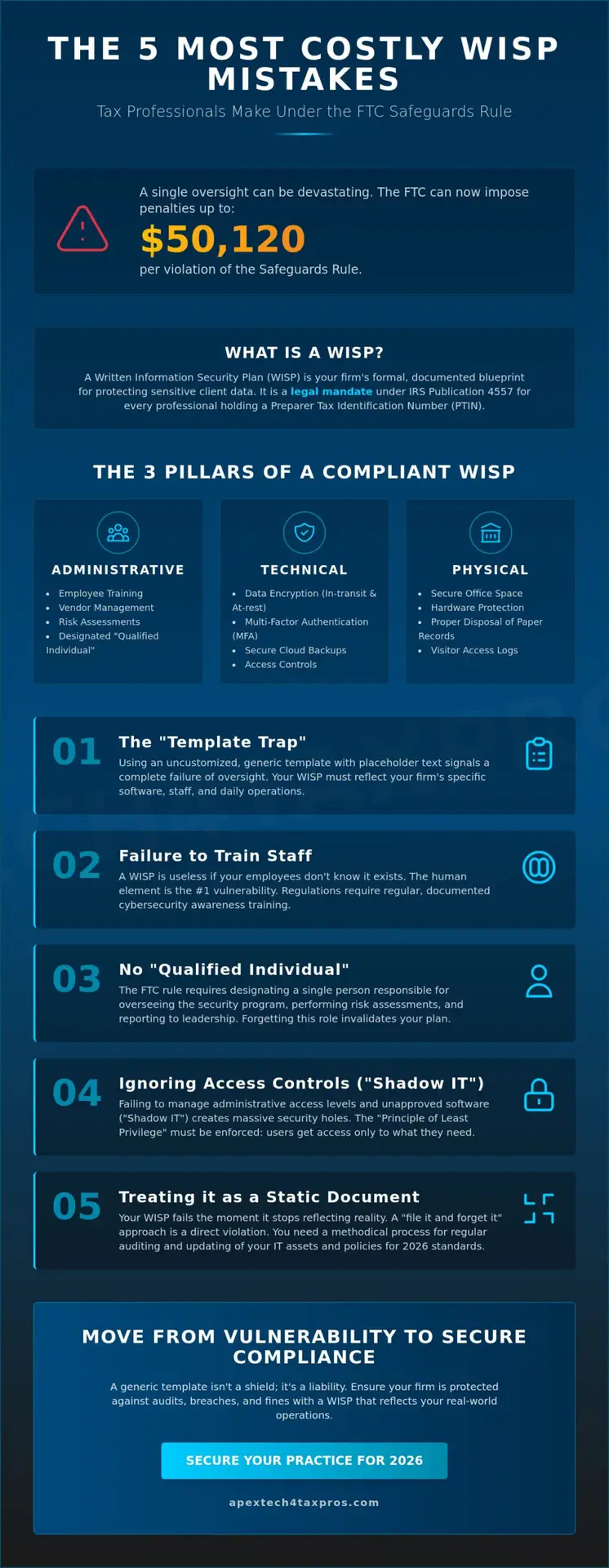

A Written Information Security Plan (WISP) is the formal, documented blueprint for how your firm protects sensitive taxpayer data. Under IRS Publication 4557, this isn’t a suggestion; it’s a legal mandate for every professional holding a Preparer Tax Identification Number (PTIN). Many practitioners view security through a general lens, but a tax-specific WISP addresses the unique lifecycle of financial data from intake to archival. Understanding What is a WISP and Why Do Most Accounting Firms Get It Wrong? requires looking past basic IT checklists and toward the comprehensive standards set by federal law. The shift from “best practice” to “federal requirement” was solidified by the FTC Safeguards Rule, which now views accounting firms as financial institutions that must maintain rigorous data protections.

The Legal Foundation: IRS Publication 4557 and the FTC

The legal framework for tax practitioners rests on the Gramm-Leach-Bliley Act (GLBA). This act grants the FTC the authority to enforce data security standards. For the 2026 season, IRS Publication 4557 requires a three-tiered approach to safety that most generic security policies miss. These include:

- Administrative Safeguards: Documented policies for employee training and vendor management.

- Technical Safeguards: Explicit requirements for encryption, multi-factor authentication, and secure cloud backups.

- Physical Safeguards: Protocols for securing office space, hardware, and the disposal of paper records.

Failing to document each tier creates significant liability, as the IRS now requires you to confirm you have a WISP every time you renew your PTIN.

The ‘Check-the-Box’ Fallacy

The most dangerous error in the industry is the “Check-the-Box” fallacy. This occurs when a firm owner downloads a template, signs the last page, and tucks it into a drawer without changing a single operational behavior. A WISP offers zero protection during an audit or a breach if the firm’s actual daily habits don’t match the written word. One of the common wisp mistakes for accountants is neglecting to appoint a “Qualified Individual.” This person is responsible for overseeing the security program, performing risk assessments, and reporting on the plan’s effectiveness to the firm’s leadership. A finished plan is never truly finished. It’s an active cycle of assessment and adjustment. If your WISP doesn’t reflect your current software stack or your remote work policies, it’s a liability rather than a shield. We help firms move beyond static documents to create active, compliant frameworks that protect their legacy and their clients.

The 5 Most Costly WISP Mistakes Tax Professionals Make

Managing a tax practice requires meticulous attention to detail, yet the technical requirements of data security often fall through the cracks. Identifying The 5 Most Costly WISP Mistakes Tax Professionals Make is essential because federal mandates require specific, enforceable protocols rather than vague intentions. One of the most common wisp mistakes for accountants is assuming that simply possessing a document is the same as having a defense. In reality, the IRS and FTC scrutinize whether your plan is a living framework or merely a file on a shelf.

Mistake #1: The Uncustomized Template

The IRS looks for firm-specific details during any compliance review. If your documentation contains placeholder text like “[Insert Firm Name Here]” or lists software your practice doesn’t actually use, it signals a failure of oversight. This “template trap” is a significant liability because it proves the firm has not performed a genuine internal risk assessment. You must tailor your framework to your specific staff size, your physical office layout, and your unique software stack. A customized Written Information Security Plan ensures that every policy reflects the actual daily behaviors of your team.

Mistake #2: Failure to Train Staff

A WISP is functionally useless if your employees are unaware of the protocols it contains. The human element remains the most frequent point of failure in data breaches, with the financial sector seeing 65% of organizations targeted by ransomware in 2024. Federal regulations require regular, documented cybersecurity awareness training sessions to ensure every team member understands their role in protecting client data. Security culture is the bridge between policy and practice. Without this bridge, even the most sophisticated technical safeguards can be bypassed by a single accidental click on a phishing email.

Beyond these foundational errors, three other technical oversights frequently lead to compliance failures:

- Missing MFA Documentation: Many firms implement Multi-Factor Authentication (MFA) but fail to document exactly where and how it is enforced. Your WISP must specify that MFA is active on all systems containing sensitive data.

- Outdated Risk Assessments: Security is not a “one and done” task. As you adopt new technology, such as AI-powered tax research tools, your risk assessment must be updated to reflect these new vectors of potential exposure.

- Lack of Incident Response Planning: Compliance requires knowing exactly what to do after a breach occurs. If you don’t have a documented step-by-step response plan, the resulting chaos can lead to delayed notifications and higher statutory fines.

Correcting these common wisp mistakes for accountants is not just about avoiding penalties; it’s about providing the protective reassurance your clients expect when they trust you with their financial lives. Moving from a generic approach to a specialized, mission-driven security framework is the only way to ensure your firm remains resilient against the evolving threat landscape of 2026.

Static Documentation vs. Active Security: The Compliance Gap

A significant number of regulatory failures stem from the disconnect between a firm’s written policies and its actual technical environment. The IRS focuses heavily on the implementation of your security plan, not just the existence of a signed PDF file. If your documentation claims that all data is encrypted at rest, but your staff uses unencrypted local drives for overflow work, your plan is functionally void. Bridging this gap requires a methodical approach to aligning your Written Information Security Plan with your daily IT infrastructure. This alignment is a core responsibility of the “Qualified Individual,” a role mandated by the FTC Safeguards Rule to oversee and maintain active security measures throughout the year.

Shadow IT remains one of the most persistent common wisp mistakes for accountants. This occurs when employees use unauthorized applications or personal cloud storage accounts to manage client files because they find the firm’s official tools cumbersome. If an app isn’t listed in your WISP, it hasn’t been vetted for compliance with the Gramm-Leach-Bliley Act. This lack of oversight creates an unmonitored entry point for cybercriminals. To maintain a state of secure compliance, you must ensure that every tool used to process taxpayer data is explicitly documented and regularly audited for security vulnerabilities.

Inventory Management: Beyond the Spreadsheet

Federal standards require a comprehensive inventory of every device that touches taxpayer data. This list must extend beyond office workstations to include mobile phones, tablets, and home computers used by remote staff. Managing “Bring Your Own Device” (BYOD) policies is a critical component of How to Audit and Update Your WISP for 2026 Standards. Your documentation must account for the entire lifecycle of these assets. This includes the initial security configuration, the monitoring of access levels, and the eventual secure disposal of hardware to prevent data remnants from falling into the wrong hands.

Software and Third-Party Vendor Risks

Your security is only as strong as the vendors you choose. Assessing the security of your tax preparation software and cloud storage providers is a mandatory step in any professional risk assessment. You are legally required to perform due diligence on all service providers who handle sensitive financial information. This documentation should confirm that your vendors comply with the same Safeguards Rule standards that apply to your firm. Establishing these expectations through written contracts ensures that your protective perimeter extends to the cloud, providing the peace of mind that your client data is in safe, capable hands across all platforms.

How to Audit and Update Your WISP for 2026 Standards

Annual compliance is not a suggestion; it’s a requirement of the FTC Safeguards Rule. To remain compliant for the 2026 filing season, you must update your documentation to reflect the August 2024 changes in Publication 5708. Start by performing a comprehensive IT asset inventory. This ensures every piece of hardware and software is accounted for before the tax rush begins. Reviewing administrative access levels is equally vital. By adhering to the Least Privilege Principle, you ensure that staff members only have access to the data necessary for their specific roles. This limits the internal exposure of a potential credential compromise.

Conducting a fresh risk assessment is the next critical step. This process identifies new vulnerabilities introduced by recent technology adoptions or changes in remote work configurations. Verification of data encryption standards is also mandatory. Your WISP should explicitly state that your encryption meets current NIST guidelines for data at rest and in transit. One of the most common wisp mistakes for accountants is failing to document the completion of the 2026 security curriculum. It isn’t enough to train your staff. You must have signed records proving they’ve completed the latest training to satisfy an IRS auditor. If you need a starting point for these requirements, our Risk Assessments provide the professional clarity needed to identify gaps in your current framework.

The Annual Review Checklist

When meeting with your IT provider, ask specific questions about your firewall logs and patch management schedules. You must document “material changes” in your business operations. These changes include hiring new contractors, adopting AI tools, or switching to different cloud-based tax software. To prove ongoing compliance during an IRS review, ensure every update is signed and dated by your firm’s Qualified Individual. This creates a clear paper trail of your commitment to data protection.

Testing Your Incident Response Plan

A plan that exists only on paper is a liability. You need a practiced response. Conduct a tabletop exercise where you simulate a ransomware attack. This helps your team understand their roles and identifies gaps in your communication strategy. Ensure your contact lists for the IRS, state authorities, and insurance providers are current. A swift response can mitigate the average cost of a data breach, which remains significantly higher for organizations with poor regulatory compliance. Practicing these scenarios ensures that if a crisis occurs, your firm is prepared to act with clinical precision rather than panic.

Beyond the Template: Securing Your Practice with Apex Tech 4 Tax Pros

A generic template might provide a starting point, but it rarely survives the scrutiny of a federal audit. Your firm’s Electronic Filing Identification Number (EFIN) is its lifeblood. Protecting it requires more than a signature on a PDF. At Apex Tech 4 Tax Pros, we recognize that avoiding common wisp mistakes for accountants is about more than just checking boxes. It’s about building a resilient infrastructure that mirrors your firm’s specific workflows and risk profile. We bridge the critical gap between complex tax law and high-level information technology to ensure your practice remains both compliant and operational. Common wisp mistakes for accountants often stem from a lack of technical oversight, which is why a professionally engineered plan is the only way to guarantee true protection.

Our “Done-For-You” approach removes the technical burden from your shoulders during the high-pressure tax season. We provide comprehensive Risk Assessments that identify vulnerabilities before they can be exploited by cybercriminals. Additionally, our Cybersecurity Awareness Training ensures your staff becomes your strongest line of defense rather than your greatest liability. By securing your practice with professional expertise, you protect your professional reputation and ensure that your client data remains in safe, capable hands. We manage the heavy lifting of compliance so you can focus on the success of your clients.

Our Multi-Disciplinary Protection Model

We combine deep federal regulatory knowledge with decades of technical expertise. This dual identity allows us to address the “Qualified Individual” requirements mandated by the FTC Safeguards Rule. Most accounting firms struggle to appoint an internal staff member with the necessary technical depth to fulfill this role. We step in as your specialized partner, managing the administrative, technical, and physical safeguards required by law. Our mission-driven approach provides the supportive security tax practitioners need to navigate an increasingly hostile digital landscape. We don’t just provide documents; we provide a disciplined and vigilant defense for your entire practice.

Take the First Step Toward Compliance

Securing your legacy shouldn’t be a source of constant anxiety. Apex Technology Management brings a long-standing heritage of technical excellence to the accounting industry. We understand the high-stakes environment of tax preparation and the clinical precision required for federal compliance. We invite you to move beyond the uncertainty of generic templates and embrace a professional security framework engineered specifically for your niche. Schedule your customized WISP consultation today to ensure your firm is fully protected for the 2026 season and beyond.

Protecting Your Practice for the 2026 Filing Season and Beyond

Maintaining a Written Information Security Plan is an active commitment that distinguishes a secure practice from a vulnerable one. You’ve learned that static templates often lead to compliance gaps and that the human element requires documented, ongoing training. Addressing the common wisp mistakes for accountants ensures your firm meets the rigorous standards of IRS Publication 4557 and the FTC Safeguards Rule. Our mission is to provide the protective reassurance you need to focus on your clients while we handle the complexities of data protection with clinical precision.

With decades of experience in niche financial IT security, we provide the specialized expertise needed to navigate these complex federal requirements. Our comprehensive risk assessments and staff training programs are specifically engineered to bridge the gap between tax law and technical infrastructure. You don’t have to carry this regulatory burden alone. Secure your firm’s future with a customized WISP from Apex Tech 4 Tax Pros. Taking these proactive steps today will grant you the peace of mind that your client data is in safe, capable hands throughout the coming year.

Frequently Asked Questions

Is a free WISP template enough to satisfy the IRS?

A free template is merely a foundational starting point and is rarely enough to satisfy an IRS auditor on its own. Federal regulations require that your plan reflects the actual, daily operations of your specific practice. Relying solely on an unedited document is one of the most common wisp mistakes for accountants because it fails to account for your unique software stack, physical office security, and specific employee protocols.

How often does an accounting firm need to update its WISP?

You should review and update your Written Information Security Plan at least once a year or whenever a material change occurs in your business. Material changes include adopting new cloud software, hiring additional staff, or transitioning to a remote work model. Regular updates are essential to ensure your security framework remains effective against the sophisticated AI-powered phishing threats emerging in 2026.

What are the penalties for not having a WISP in 2026?

Non-compliance with the FTC Safeguards Rule can result in civil penalties of up to $50,120 per violation. In addition to federal fines, state-level authorities may impose their own sanctions, such as California’s penalties for firms lacking a documented incident response plan. Perhaps most critically, the IRS may choose to suspend your EFIN, which effectively prevents you from filing tax returns for your clients.

Who is a ‘Qualified Individual’ according to the FTC Safeguards Rule?

The Qualified Individual is a designated person responsible for overseeing, implementing, and enforcing your firm’s information security program. While this person does not need a specific certification, they must have the technical competency to manage your security risks. This individual is required to perform regular risk assessments and provide the firm’s leadership with written reports regarding the overall effectiveness of the security plan.

Does a solo practitioner still need a Written Information Security Plan?

Every tax professional holding a PTIN is legally required to maintain a WISP, regardless of the size of their practice. The IRS and FTC do not provide exemptions for solo practitioners or small home-based offices. Because you handle sensitive financial data, you must document how you apply administrative, technical, and physical safeguards to protect that information from unauthorized access or accidental disclosure.

What should be included in a WISP incident response plan?

Your incident response plan must outline the specific steps your firm will take to identify, contain, and mitigate the impact of a security event. It should include a current contact list for the IRS, state taxing authorities, and your cyber insurance provider. Having these procedures documented in advance is critical for complying with the FTC notification requirements that mandate reporting certain breaches within 30 days of discovery.

How does IRS Publication 4557 differ from the FTC Safeguards Rule?

IRS Publication 4557 is a guide specifically tailored to help tax professionals understand their data protection obligations, whereas the FTC Safeguards Rule is the actual federal regulation that carries the force of law. Publication 4557 provides a roadmap for meeting the standards set by the Gramm-Leach-Bliley Act. Both emphasize that a Written Information Security Plan is a mandatory legal requirement for anyone in the tax industry.

Can my IT company write my WISP for me?

An IT provider can provide the technical data for your plan, but the firm’s leadership is ultimately responsible for its accuracy and implementation. A frequent error among common wisp mistakes for accountants is assuming a general IT provider understands the specific regulatory nuances of the tax profession. It’s often more effective to partner with a specialized firm that understands both technical infrastructure and IRS compliance standards.