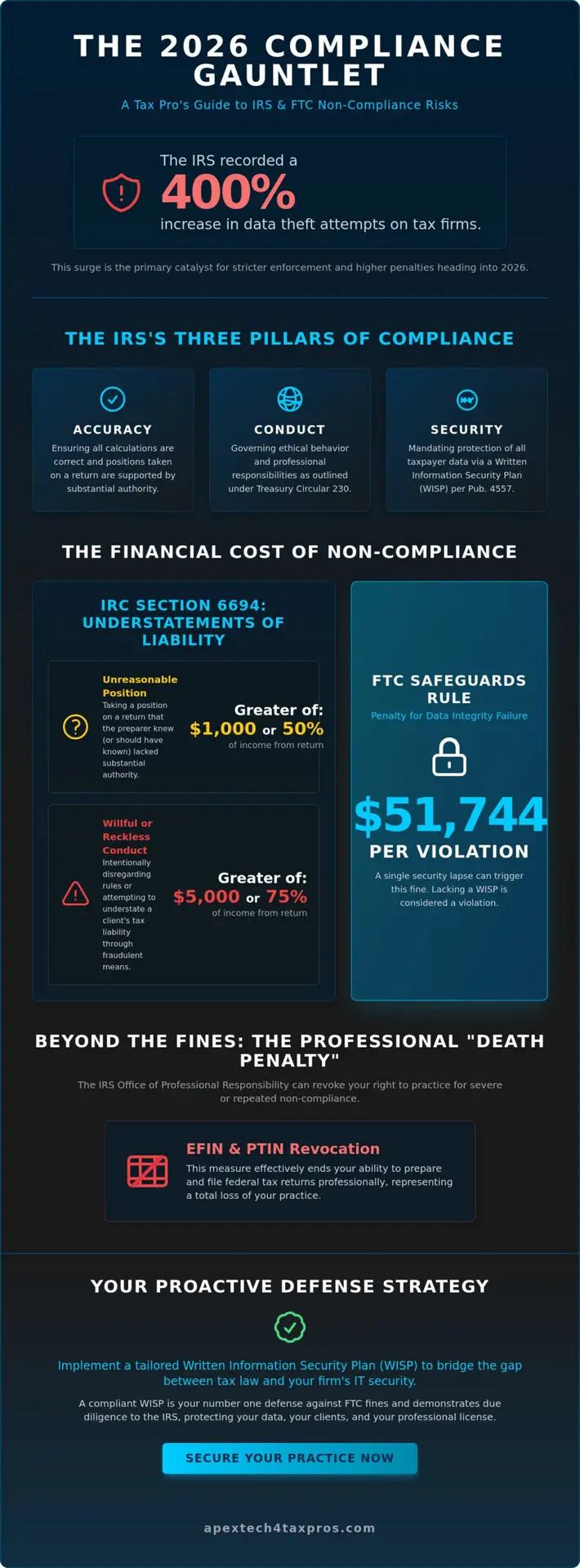

The IRS recorded a 400 percent increase in data theft attempts targeting tax firms during the 2024 season, which serves as the primary catalyst for the stricter enforcement of irs non-compliance fines entering 2026. You’ve likely felt the mounting pressure of these shifting regulations, especially as the distinction between a client’s tax error and your own professional liability becomes increasingly technical. It’s difficult to balance the demands of a busy firm with the complex mandates of the FTC Safeguards Rule. We know you value the integrity of your practice above all else; the fear of a PTIN or EFIN suspension shouldn’t be your primary motivator for information security.

This guide offers a clinical look at the 2026 penalty amounts and the specific professional risks facing practitioners today. I’ll show you exactly how to bridge the gap between your current workflows and the rigorous standards of IRS Publication 4557. We’ll examine the specific components of a compliant Written Information Security Plan (WISP) and provide a roadmap to secure your data. This analysis will help you protect your professional license, allowing you to operate with the confidence that comes from total regulatory alignment and proven technical safeguards.

Key Takeaways

- Navigate the shifting 2026 regulatory environment to understand how IRC Sections 6694 and 6695 determine the severity of irs non-compliance fines for your practice.

- Evaluate the financial risks of the FTC Safeguards Rule, where a single data integrity failure can result in penalties reaching $51,744 per violation.

- Protect your professional standing by recognizing the triggers for EFIN and PTIN revocation, the “death penalty” measures handled by the IRS Office of Professional Responsibility.

- Implement a proactive defense strategy using a tailored Written Information Security Plan (WISP) to bridge the gap between tax law requirements and your firm’s IT security.

Understanding the Landscape of IRS Non-Compliance Fines for Practitioners in 2026

Practitioner non-compliance represents a failure to meet the Treasury’s professional conduct or data security standards. It’s vital to distinguish between taxpayer penalties, such as failure to pay or late filing, and the specific irs non-compliance fines levied against professionals for preparer misconduct. While a taxpayer might face interest on a late payment, a practitioner faces direct financial sanctions for failing to uphold their fiduciary and technical duties. You can find a broader context of these distinctions in this IRS Penalties Overview, which outlines the foundational structure of federal tax enforcement.

The 2026 tax season marks a turning point in federal oversight. The IRS has shifted its focus heavily toward ‘Return Preparer Fraud’ and ‘Data Safeguards’ following the 2024 Strategic Operating Plan update. This initiative aims to protect the integrity of the tax system by enforcing three pillars of compliance: Accuracy, Professional Conduct, and Information Security. Accuracy ensures the math is correct, Professional Conduct governs ethical behavior under Circular 230, and Information Security mandates the protection of taxpayer data from cyber threats.

The Role of IRS Publication 4557 in 2026

IRS Publication 4557 remains the definitive benchmark for what the agency considers ‘reasonable’ security measures. It connects tax preparation directly to the FTC Safeguards Rule, mandating that every practitioner protects taxpayer data with technical and administrative controls. By 2026, the IRS has removed the ‘ignorance’ loophole. “I didn’t know” doesn’t work as a defense when you’re facing irs non-compliance fines. If your firm lacks a tailored Written Information Security Plan (WISP), you’re technically non-compliant before you even file your first return of the season.

Who is at Risk? From Solo Practitioners to Large Firms

The IRS monitors PTIN holders and Electronic Return Originators (EROs) with increasing precision through automated data matching. Small firms have become primary targets for compliance audits because they often lack the technical infrastructure of larger entities. No firm is too small for scrutiny. In this digital-first environment, the cost of negligence is escalating. Data from 2025 indicated that even minor security lapses led to penalties exceeding $10,000 per incident in some jurisdictions. Bridging the gap between tax knowledge and IT security is no longer optional; it’s a requirement for survival. Practitioners must realize that their regulatory burdens are understood by the agency, and the safe handling of sensitive data is the only way to maintain professional standing.

The Financial Cost of Misconduct: Tax Preparer Penalties Explained

The IRS holds the architects of tax returns to a rigorous standard of accuracy and ethics. Understanding irs non-compliance fines requires a deep dive into the Internal Revenue Code (IRC), which distinguishes between simple procedural errors and intentional fraud. For the 2026 filing season, the IRS has adjusted penalty amounts to account for inflation, making the cost of oversight higher than ever for practitioners who fail to maintain strict data integrity and reporting standards.

IRC Section 6694: Understatements of Liability

This section of the code focuses on the quality of the positions taken on a return. If a preparer takes an “unreasonable position” that leads to an understatement of tax, the penalty is the greater of $1,000 or 50% of the income derived from the return. This standard applies when the preparer knew, or should have known, that the position lacked substantial authority. It is a objective test based on professional standards rather than intent.

The stakes rise significantly for conduct deemed “willful or reckless.” If the IRS determines a preparer intentionally disregarded rules or attempted to understate liability through fraudulent means, the fine jumps to the greater of $5,000 or 75% of the income earned from that return. To avoid these assessments, you must document your due diligence meticulously. Keeping a clear trail of taxpayer interviews and verified source documents proves you performed the necessary checks to validate the information provided by the client.

IRC Section 6695: Procedural and Administrative Fines

While Section 6694 targets the substance of a return, Section 6695 enforces the administrative guardrails of the profession. These fines are often assessed per occurrence, which means they can aggregate into substantial sums for high-volume firms. For the 2026 tax year, common procedural failures include:

- Failure to sign a return or provide a copy: Projected at $65 per violation, with an annual cap of approximately $33,000.

- Failure to retain records: Practitioners must keep a list of taxpayers or copies of returns for three years. Failure to do so results in a $65 fine per return.

- Negotiating a refund check: Endorsing or otherwise negotiating a taxpayer’s refund check is a critical violation, with fines projected at $640 per check.

- Due Diligence failures: Failing to meet the four-part due diligence requirements for the EITC, Child Tax Credit, or Head of Household status carries a projected fine of $640 per failure.

Protecting your practice requires more than just tax knowledge; it requires robust internal systems. Implementing a tailored Written Information Security Plan (WISP) helps ensure that the records you’re required to retain under Section 6695 remain secure and accessible during a potential IRS investigation. These administrative fines are often the easiest for the IRS to assess because they rely on objective evidence of missing signatures or incomplete files.

The ‘New’ Non-Compliance: Data Security and the Safeguards Rule

Historically, a cyberattack was viewed as a misfortune. Today, the IRS and FTC view it as a failure of regulatory duty. Under the updated FTC Safeguards Rule, tax practitioners face severe financial penalties for failing to protect non-public personal information. A single violation can trigger a fine of up to $51,744. These irs non-compliance fines aren’t just one-time penalties; they apply per instance of negligence. The IRS now bridges the gap between tax law and cybersecurity by requiring practitioners to certify their compliance during the annual EFIN application and renewal process. If you can’t prove you’ve implemented specific security measures, your ability to file returns electronically is at risk.

The financial impact extends far beyond the initial government penalty. A data breach forces a firm into a state of emergency that carries heavy hidden costs:

- Forensic Audits: These investigations often cost upwards of $20,000 to identify which taxpayer files were accessed.

- Legal Fees: Specialized counsel is required to navigate federal reporting requirements.

- Client Notification: Printing and mailing legally mandated breach notices can cost between $150 and $200 per client.

The Mandatory Written Information Security Plan (WISP)

Every tax professional must maintain a tailored WISP to retain their EFIN in 2026. This isn’t a suggestion. It’s a federal requirement under IRS Publication 5708. The IRS looks for specific components during an audit, including a designated program coordinator, a risk assessment report, and regular employee training logs. Many firms make the mistake of downloading a generic template and never filling in the blanks. A template that doesn’t reflect your actual network architecture or office procedures won’t protect you from irs non-compliance fines during a regulatory review. It’s about data integrity, not just checking a box.

Consequences of a Data Breach for Tax Firms

When a breach occurs, the IRS immediately monitors for compromised PTINs to prevent fraudulent filings. This triggers a cascade of expensive obligations. You’ll likely face forensic audit costs that often exceed $20,000 to determine the extent of the exposure. State-level data privacy laws, such as the CCPA or similar mandates in all 50 states, require immediate client notification. These letters and the associated legal counsel can cost a firm between $150 and $200 per affected client. Tax professionals hold a non-delegable duty of care to implement reasonable administrative, technical, and physical safeguards that ensure the confidentiality of taxpayer records.

Beyond the Fines: Losing Your Right to Practice

Monetary penalties hurt your firm’s bottom line, but the administrative “death penalty” destroys your business entirely. When the IRS moves beyond irs non-compliance fines and targets your professional credentials, the damage is often irreversible. A single compliance failure, such as a breach of the data security standards outlined in IRS Publication 1345, can lead to the immediate revocation of your Electronic Filing Identification Number (EFIN) and Preparer Tax Identification Number (PTIN). Without these, you cannot legally operate as a tax professional.

EFIN Suspension and Revocation

Electronic filing is a privilege, not a right. The IRS follows a strict process when it suspects a practitioner has compromised the integrity of the e-file system. This process often begins with a formal letter of suspension, but severe security failures can trigger an immediate shutdown of filing privileges. Because the IRS processed over 160 million individual income tax returns electronically in 2023, losing your EFIN effectively closes your practice overnight. Reinstating a revoked EFIN is a grueling process that requires a full audit of your internal systems and proof that you’ve implemented a compliant Written Information Security Plan (WISP). Most firms don’t survive the downtime during this investigation.

OPR Sanctions and Circular 230

The Office of Professional Responsibility (OPR) serves as the primary watchdog for tax practitioner conduct. It enforces the standards found in Treasury Department Circular 230, which governs the practice of CPAs, attorneys, and Enrolled Agents. If the OPR determines your firm has engaged in “disreputable conduct” or failed to exercise due diligence, they can issue sanctions that range from a private censure to full disbarment from practice. These actions are not private. The IRS publishes the names of sanctioned practitioners in the Internal Revenue Bulletin every quarter, creating a permanent public record that erodes client trust. While you can eventually pay off irs non-compliance fines, you can’t easily repair a reputation damaged by a public IRS sanction.

Protecting your practice requires more than just accurate math; it requires a specialized approach to regulatory data standards. To safeguard your credentials, you must ensure your technology environment meets every federal mandate. Learn how we help you bridge the gap between tax preparation and IT security to keep your EFIN and your reputation secure.

A Proactive Compliance Strategy: Protecting Your Practice with Apex Tech

Apex Tech 4 Tax Pros operates as a Dual-Expert Guardian. We’ve spent over 20 years bridging the gap between technical IT security and the complex world of tax law. This specialized focus is vital because the IRS has signaled a move toward stricter enforcement of the FTC Safeguards Rule. By 2026, firms lacking a robust security posture will face increased scrutiny. We provide the protective reassurance you need to focus on your clients while we handle the regulatory heavy lifting. A customized Written Information Security Plan (WISP) serves as your primary defense during an audit. It proves you’ve taken the necessary steps to protect taxpayer data, effectively shielding you from heavy irs non-compliance fines.

Annual risk assessments are a mandatory component of modern practice management. These aren’t just checkboxes; they’re deep dives into your firm’s digital health. According to the 2022 Verizon Data Breach Investigations Report, 82% of breaches involved a human element. This makes staff training a non-negotiable requirement under the Safeguards Rule (16 CFR Part 314). We help you identify compliance gaps before they turn into costly liabilities. Our approach ensures your firm remains disciplined, vigilant, and fully aligned with federal expectations.

The Apex Tech 4 Tax Pros Solution

We develop tailored WISPs specifically for the accounting industry’s unique workflows. Our risk assessments mirror the exact scrutiny of an IRS compliance check, ensuring no vulnerability goes unnoticed. We also prioritize data integrity through secure cloud backups. This ensures practice continuity even in the event of a localized hardware failure or cyberattack. You’ll have peace of mind knowing your firm’s records are safe, accessible, and compliant with all current standards.

Steps to Take Today to Avoid 2026 Fines

The window for preparation is closing. Firms that wait until 2026 to update their protocols will likely fall behind. You can protect your revenue and reputation by taking these concrete steps now:

- Conduct an immediate audit of your current security documentation to ensure it meets the latest IRS Publication 4557 standards.

- Schedule recurring staff training sessions to mitigate the risk of “human error” breaches.

- Consult with a dual-expert firm to ensure your IT infrastructure and regulatory documentation are perfectly aligned.

- Review your encryption protocols for all outbound client communications to prevent data interception.

Proactive management is the only way to stay ahead of evolving irs non-compliance fines. Don’t leave your practice’s survival to chance. Taking action today establishes a foundation of security that lasts for years. You can secure your firm’s future with a professional WISP assessment to ensure you’re fully prepared for the challenges ahead.

Securing Your Practice Against 2026 Regulatory Shifts

The 2026 landscape for tax practitioners demands more than just accurate returns. It requires rigorous adherence to the IRS Safeguards Rule and mandatory Written Information Security Plans. Failing to meet these standards leads to severe irs non-compliance fines and the potential loss of your EFIN. Since the FTC updated 16 C.F.R. Part 314 requirements for non-banking financial institutions, the margin for error has vanished. You can’t afford to treat data security as a secondary concern when your professional license is on the line.

Apex Tech 4 Tax Pros brings 20 years of specialized experience to your practice. As a family-owned boutique firm, we take personal accountability for your data integrity. We’ve spent two decades bridging the gap between tax preparation and IT security to ensure your office stays operational and compliant. We understand the specific pressures you face during peak season and provide the tailored support needed to mitigate risks before they become penalties. Protect your practice from IRS fines: Download our FREE WISP Template or schedule a professional assessment today. You’ve built a reputation on trust; let’s work together to keep it that way.

Frequently Asked Questions Regarding IRS Practitioner Penalties

What is the maximum fine for a tax preparer under IRC Section 6694?

Under IRC Section 6694, the maximum fine for a willful or reckless understatement of a client’s tax liability is the greater of $5,000 or 75% of the income the practitioner earned from the return. If the understatement results from an unreasonable position without a willful intent to underpay, the penalty is $1,000 or 50% of the derived income. These irs non-compliance fines ensure that practitioners maintain high regulatory standards during every filing season.

Can the IRS fine me if I don’t have a Written Information Security Plan (WISP)?

The IRS can’t always levy a direct “WISP fine,” but they can suspend your EFIN and refer your firm to the FTC for Safeguards Rule violations. Since June 9, 2023, the federal government has mandated that all financial institutions, including tax preparers, maintain a Written Information Security Plan. We focus on bridging the gap between your tax expertise and these technical requirements by providing a tailored WISP that meets these specific federal mandates.

What happens if a tax professional’s EFIN is suspended due to non-compliance?

If your Electronic Filing Identification Number (EFIN) is suspended, you lose your ability to transmit electronic returns to the IRS immediately. This suspension effectively shuts down your business operations, as the IRS requires e-filing for practitioners who prepare more than 10 returns annually. You’ll receive a formal notice from the IRS e-file Provider Program, and you typically have 30 days to file an appeal before the suspension becomes permanent.

Are IRS non-compliance fines tax-deductible for my business?

IRS non-compliance fines aren’t tax-deductible for your business under Internal Revenue Code Section 162(f). This federal law prohibits any deduction for payments made to a government entity due to a violation of any law. Because these penalties are considered punitive rather than ordinary business expenses, your firm must pay them using after-tax dollars. This lack of deductibility significantly increases the true financial burden of any assessed penalty on your practice.

How much does the FTC fine tax firms for Safeguards Rule violations in 2026?

The FTC can assess civil penalties of up to $51,744 per violation of the Safeguards Rule, based on the inflation adjustments established in early 2024. By 2026, this amount is expected to increase further through annual adjustments required by the Federal Civil Penalties Inflation Adjustment Act. A single data breach involving multiple clients can result in cumulative fines that quickly exceed the annual revenue of a localized, family-owned tax firm.

What should I do if I receive a notice of a practitioner compliance audit?

You should immediately contact your legal counsel and organize your Written Information Security Plan (WISP) along with all internal compliance records. The IRS Office of Professional Responsibility (OPR) conducts these audits to ensure you’re following Circular 230 regulations. Having a tailored documentation trail ready for review within 10 days of the notice shows the IRS that you take data integrity and your role as a trusted advisor seriously.

Does professional liability insurance cover IRS non-compliance fines?

Most professional liability insurance policies don’t cover IRS fines or government-imposed penalties. While these policies protect your firm against client lawsuits for errors and omissions, they specifically exclude punitive assessments from federal agencies like the IRS or FTC. You’ll find this exclusion in the “Fines and Penalties” section of your policy. It’s vital to maintain strict compliance because your insurance carrier won’t reimburse you for these specific regulatory costs.

How often does the IRS update practitioner penalty amounts?

The IRS updates practitioner penalty amounts annually to account for inflation. These updated figures are typically released in a Revenue Procedure during the fourth quarter of the year preceding the change. For example, the 2026 penalty rates were established by the IRS in late 2025. This annual cycle ensures that the financial deterrents remain effective as the economic environment changes, making it necessary for you to review compliance standards every year.