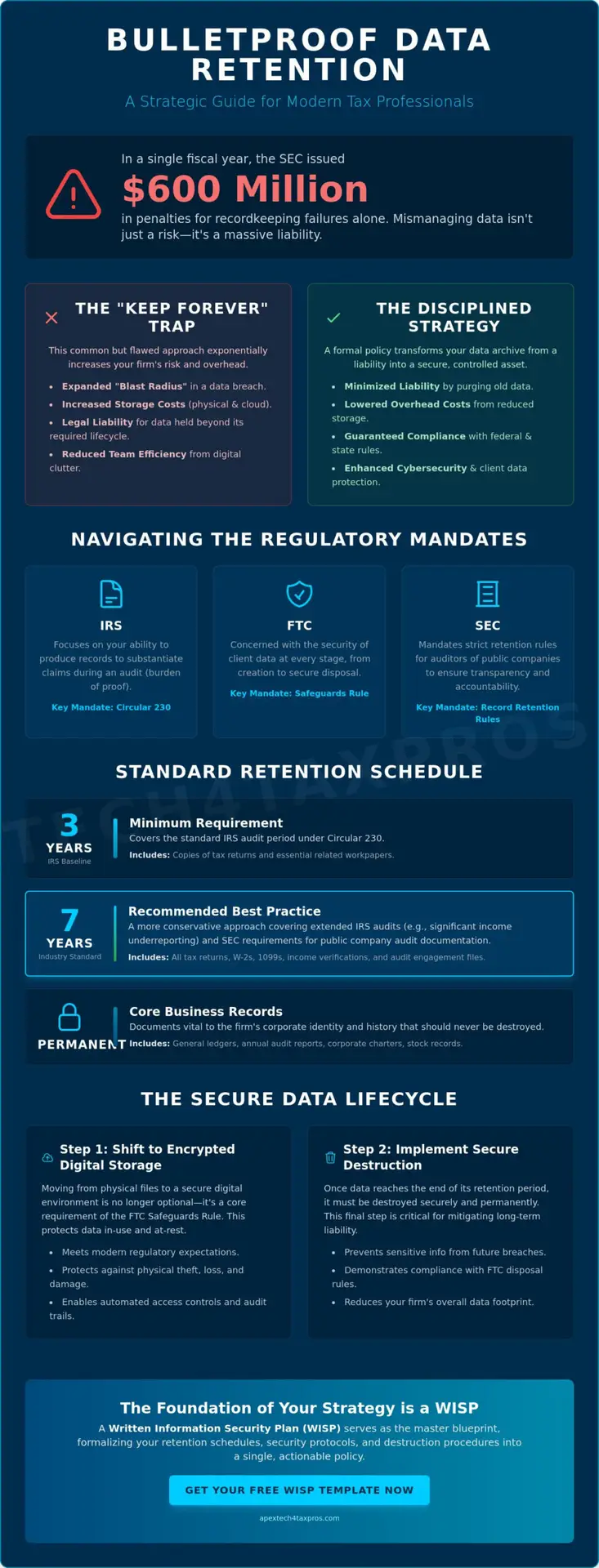

Did you know the SEC ordered $600 million in penalties for recordkeeping failures in a single fiscal year? For many practitioners, the fear of an IRS audit is only eclipsed by the anxiety of a data breach involving archived files. You likely feel the weight of these overlapping regulations while trying to build a compliant data retention policy for accounting firms. It’s a high-stakes environment where a single missing document or an improperly discarded folder leads to devastating consequences.

We understand that navigating these mandates feels like aiming at a moving target, especially with new state privacy laws taking effect in 2026. This guide will help you master the complex intersection of IRS recordkeeping rules and the FTC Safeguards Rule to build a bulletproof strategy. You’ll gain a clear retention schedule for every document type while learning how to minimize liability through disciplined data destruction. We’ll provide a methodical path to ensure your firm remains both compliant and protected against modern threats.

Key Takeaways

- Understand the specific retention timelines required by the IRS and SEC to ensure your firm remains audit-ready and compliant with federal mandates.

- Learn how to develop a data retention policy for accounting firms that satisfies the rigorous cybersecurity standards set by the FTC Safeguards Rule.

- Discover why shifting from physical filing to encrypted digital environments is essential for meeting modern regulatory expectations for data protection.

- Identify the critical steps for secure data destruction to mitigate liability and prevent sensitive information from falling into the wrong hands after its retention period ends.

- See how a customized Written Information Security Plan (WISP) serves as the foundation for an automated, secure, and resilient data management strategy.

What is a Data Retention Policy for Accounting Firms?

A Data retention policy is far more than a simple schedule of dates. It’s a formal, strategic document that governs how your firm stores, protects, and eventually destroys sensitive client information. For tax professionals, this policy serves as the bridge between two critical federal mandates: IRS Publication 4557 and the FTC Safeguards Rule. While the IRS focuses on your ability to produce records during an audit, the FTC is concerned with the security of that data at every stage of its existence. Within your broader Written Information Security Plan (WISP), the retention policy acts as the operational manual for data lifecycle management.

Many firms fall into the trap of “keeping everything forever” out of a misplaced sense of caution. This approach is a significant legal and cybersecurity liability. Every byte of data you retain beyond its required lifecycle is a potential target. If a breach occurs, you’re legally responsible for all compromised files, including those that should’ve been destroyed years ago. A robust data retention policy for accounting firms transforms your archive from a growing liability into a controlled, secure asset.

The Legal Mandate for Data Retention

The IRS operates on the principle of “burden of proof.” This means the responsibility to substantiate every claim on a tax return falls on the taxpayer and, by extension, their representative. This necessitates a baseline retention period, typically three to seven years depending on the document type. However, the regulatory environment is shifting. The FTC Safeguards Rule now explicitly requires firms to have documented procedures for the secure disposal of customer information. You must also account for state-specific mandates. For instance, new privacy laws taking effect in 2026 in states like Indiana and Kentucky may impose stricter requirements than federal baselines. Your data retention policy for accounting firms must reconcile these conflicting timelines into a single, actionable workflow.

Benefits of a Disciplined Retention Strategy

Implementing a rigorous schedule offers immediate operational advantages. First, it significantly reduces your “blast radius.” If a cybercriminal gains access to your systems, they can only steal what’s currently stored. By purging expired records, you limit the scope of potential damage. Second, efficiency improves when your team isn’t digging through decades of digital clutter to find a single 2024 workpaper. Finally, there’s a clear financial incentive. Whether you’re paying for on-site mobile shredding or secure cloud storage, reducing the volume of data you manage directly lowers your overhead costs. A disciplined strategy ensures that your firm remains lean, compliant, and focused on the future.

The 2026 Accounting Records Retention Schedule

Establishing a standard data retention policy for accounting firms requires a tiered approach that recognizes the varying lifecycles of financial data. You cannot treat a casual internal memo with the same gravity as a signed corporate tax return. For most firms, the “Three-Year Rule” serves as the foundational baseline. Under Circular 230, tax preparers must retain copies of tax returns and related documents for at least three years. This window aligns with the standard IRS audit period. However, many practitioners adopt a more conservative “Seven-Year Rule” to account for the extended six-year audit window triggered by significant income underreporting.

Certain records demand even greater longevity. Auditors of public companies, for instance, must adhere to SEC record retention rules, which mandate a seven-year retention period for audit documentation following the conclusion of an engagement. Beyond these mandates, your firm should identify “permanent” records that are never destroyed. These include general ledgers, annual audit reports, and corporate charters. Maintaining this hierarchy ensures your firm remains audit-ready without drowning in unnecessary digital clutter.

Client Tax Records and Supporting Documents

Individual and corporate tax returns generally follow the seven-year recommendation to ensure safety against extended audits. This includes all supporting documentation such as 1099s, W-2s, and income verification files. Special care is required for clients with net operating losses (NOLs) or tax credit carryforwards. In these instances, you must keep records until the loss or credit is fully utilized, plus the additional three-to-seven-year statute window. If you’re looking to formalize these timelines, starting with a FREE WISP Download Template can help you document your firm’s specific commitments.

Internal Firm Financial and Personnel Records

Your internal operations carry their own regulatory weight. While the Fair Labor Standards Act requires keeping payroll records for three years, the IRS mandates a four-year minimum for employment tax records. We recommend standardizing your accounts payable and receivable ledgers to a seven-year schedule to match your tax filings. Legal correspondence and accident reports should often be kept longer, typically based on your state’s specific statute of repose for professional liability claims.

Statutes of Limitations and Exceptions

The IRS can look back further than the standard three years if a taxpayer underreports their gross income by more than 25%. In cases of suspected fraud or where no return was filed, there is no statute of limitations at all. A statute of limitations for federal tax audits is the legally defined period during which the IRS can assess additional tax or initiate a formal investigation into a filed return. Your data retention policy for accounting firms must account for these “look-back” exceptions to protect both your firm and your clients from unexpected litigation.

Securing the Archive: Digital vs. Physical Retention

A data retention policy for accounting firms is only as strong as the infrastructure supporting it. While the previous section detailed how long you must keep specific records, the method of storage determines your firm’s actual level of risk. The transition from heavy filing cabinets to encrypted digital vaults isn’t just a matter of convenience; it’s a regulatory necessity under the FTC Safeguards Rule. This rule mandates that financial institutions, including tax preparers, protect “data at rest.” This means your archived files require the same level of rigorous security as your active client workpapers.

Relying on a single storage location is a recipe for disaster. Whether you’re facing a localized hardware failure or a sophisticated ransomware attack, your retention strategy must include redundant, Secure Cloud Backup. This ensures that even if your primary archive is compromised, your firm can fulfill its “burden of proof” obligations to the IRS without interruption. A resilient archive is one where data is not just stored, but systematically protected against every foreseeable threat.

Encryption and Access Controls for Digital Records

Basic consumer cloud storage is insufficient for sensitive taxpayer data. These platforms often lack the granular encryption and audit logging required by federal standards. To meet compliance, every digital archive must be shielded by Multi-Factor Authentication (MFA). This simple step prevents unauthorized access even if credentials are stolen. Additionally, performing annual Risk Assessments is vital to identify vulnerabilities in your digital vault before they’re exploited. Your data retention policy for accounting firms should explicitly define who has access to archived data and under what specific circumstances that access is granted.

The Problem with Legacy Physical Records

Paper records represent a unique security liability because they cannot be encrypted. Phasing out legacy paper files reduces the physical “attack surface” of your office. If you must maintain physical archives, ensure the storage facility meets IRS security standards, including controlled access, fire suppression, and climate monitoring to prevent document degradation. When transporting sensitive documents to off-site storage, always use secure, tracked containers and verified couriers. We often recommend that firms integrate Cybersecurity Awareness Training into their workflow so staff understand that data protection applies to the box in the hallway just as much as the file on the server. Physical security is the first line of defense in a truly comprehensive retention strategy.

Implementing a Secure Data Destruction Protocol

The final stage of the data lifecycle is often the most overlooked, yet it represents a critical point of vulnerability. While many practitioners focus on the security of active files, the liability of retaining expired data can be catastrophic. If your firm is breached, every outdated record you failed to purge becomes a liability for identity theft and a target for ransomware actors. A disciplined data retention policy for accounting firms must conclude with a rigorous destruction protocol that ensures information is not just removed, but rendered completely unrecoverable. Federal compliance standards, particularly under the FTC Safeguards Rule, define “secure destruction” as the permanent elimination of data such that it cannot be reconstructed.

To maintain consistent compliance, we recommend establishing an annual “Purge Day.” This dedicated time allows your team to audit your archives against your retention schedule and clear out records that have reached their expiration. Following this process, you should obtain or create a Certificate of Destruction (CoD). This document serves as definitive proof for your compliance file that the data was handled according to industry standards. If you’re unsure if your current disposal methods meet these high-stakes requirements, performing regular Risk Assessments can reveal hidden gaps in your end-of-life data handling.

Methods of Permanent Destruction

Physical documents require more than simple recycling; they must undergo cross-cut shredding to prevent reconstruction. Digital data presents a different challenge. Simply “deleting” a file or formatting a drive doesn’t remove the underlying data. You must use digital wiping software that meets government standards for permanent erasure. Decommissioning old hardware requires special attention too. Hard drives from retired laptops or copiers must be physically destroyed or wiped using specialized tools to ensure no residual taxpayer information remains on the platters.

Documenting the Destruction Process

A secure process is meaningless without a verifiable audit trail. Your firm should maintain a detailed destruction log that records exactly what was destroyed, the date of the action, and the identity of the person who performed it. Assigning a designated “Security Coordinator” provides a single point of accountability for this disposal process. These logs aren’t just internal records; they should be integrated into your annual IRS security peer review. By treating data destruction as a formal, documented event, you demonstrate a level of professional vigilance that protects your firm from regulatory scrutiny and legal liability.

Building Your Policy with Apex Tech 4 Tax Pros

Implementing a robust data retention policy for accounting firms is a complex undertaking that requires more than just a list of dates. It demands a technical infrastructure that can support the entire lifecycle of sensitive information. At Apex Tech 4 Tax Pros, we specialize in bridging the gap between regulatory requirements and secure operational reality. By integrating data retention into your firm’s daily DNA, we transform compliance from a seasonal burden into a resilient, automated process that protects your legacy and your clients.

Our approach begins with comprehensive Risk Assessments to identify exactly where your data lives and where it’s most vulnerable. We then provide the tools and training necessary to manage that data with clinical precision. Through our Cybersecurity Awareness Training, your staff learns to treat every document as a strategic asset and a potential liability. This ensures that retention and disposal protocols are followed without fail. We don’t just give you a policy; we provide the professional reassurance that your firm is prepared for any regulatory challenge.

Customized WISP: The Foundation of Compliance

A generic template cannot account for the specific nuances of your practice. We provide a Customized Written Information Security Plan (WISP) engineered to meet the exact needs of your firm while satisfying IRS Publication 4557 and FTC standards. This document serves as the legal foundation of your compliance. It contains specific clauses for data retention and secure disposal that are tailored to your firm’s size and client base. By consolidating these mandates into a single, authoritative plan, you provide your team with a clear roadmap for navigating high-stakes regulatory environments. It’s about moving beyond basic checklists to a sophisticated security strategy.

Secure Cloud Backup and Business Continuity

Data retention is meaningless if the information isn’t available when you need it most. Our Secure Cloud Backup solutions ensure the integrity of your records against hardware failure, natural disasters, and the growing threat of ransomware. During an IRS audit, the speed and accuracy of record retrieval are paramount. We automate the backup and retention process to provide you with an archive that is both highly accessible and strictly secure. This level of automation reduces human error and ensures that your data retention policy for accounting firms is consistently enforced without manual intervention. Secure your firm’s future with a customized WISP from Apex Tech 4 Tax Pros and gain the confidence that comes from professional, mission-driven data protection.

Securing Your Firm’s Legacy in 2026

Establishing a resilient data retention policy for accounting firms is no longer just a matter of organized filing; it’s a critical component of your firm’s total cybersecurity posture. By synchronizing your retention schedules with federal mandates and implementing secure, encrypted digital archives, you move from a state of vulnerability to one of disciplined compliance. You’ve seen that the lifecycle of data must end with a documented, permanent destruction process to truly minimize your liability and protect your clients from the growing threat of identity theft.

At Apex Tech 4 Tax Pros, we bring decades of experience protecting sensitive financial data to every engagement. Our dual identity as technical experts and regulatory insiders ensures your firm meets the rigorous standards of IRS Publication 4557 with precision. We provide the protective reassurance you need to focus on your clients while we manage the technical complexities of information security. Download your FREE WISP Template or request a customized plan today to begin building your bulletproof strategy. Your commitment to data integrity today ensures a more secure and prosperous future for your practice.

Frequently Asked Questions

How long does the IRS require accounting firms to keep client records?

The IRS generally mandates a three-year retention period for tax returns and supporting documents as this matches the standard audit window. However, most professionals advise keeping records for seven years to protect against the six-year window triggered if income is underreported by more than 25%. Maintaining a consistent data retention policy for accounting firms ensures you’re never caught without the necessary burden of proof during a federal inquiry.

What is the difference between a records retention schedule and a data retention policy?

A records retention schedule is a simple list of document types and their expiration dates, while a data retention policy is a comprehensive security document. The policy outlines the entire lifecycle of data, including storage methods, encryption standards, and secure disposal protocols. It functions as a core component of your firm’s Written Information Security Plan (WISP) rather than just a calendar of dates.

Does the FTC Safeguards Rule mandate how I destroy client data?

Yes, the FTC Safeguards Rule specifically requires firms to implement and document procedures for the secure disposal of customer information. You must ensure that the data is rendered unreadable and cannot be reconstructed. This mandate is why your data retention policy for accounting firms must include specific destruction methods like cross-cut shredding or government-grade digital wiping to remain compliant.

Can I store all my accounting records exclusively in the cloud?

You can certainly store records exclusively in the cloud as long as the provider meets professional security standards. This includes end-to-end encryption, multi-factor authentication, and redundant backups to prevent data loss. Relying on basic consumer-grade storage is risky, so you should verify that your cloud environment complies with the FTC Safeguards Rule requirements for protecting data at rest.

What happens if I destroy records before the retention period ends?

Destroying records prematurely leaves you unable to fulfill the IRS “burden of proof” requirement during an audit. If you can’t produce the supporting documentation for a deduction or credit, the IRS may disallow those items and assess additional taxes, interest, and penalties. It also creates a compliance gap under the FTC Safeguards Rule, which requires you to maintain records according to your documented plan.

How often should an accounting firm update its data retention policy?

You should review and update your policy at least once per year to ensure it reflects current federal and state regulations. For example, 2026 introduces new comprehensive data privacy laws in states like Indiana and Kentucky. Regular updates allow your firm to adapt to these changes and adjust your technical safeguards to meet evolving cybersecurity threats and storage best practices.

Is a WISP required if I only have a few clients?

Yes, a Written Information Security Plan (WISP) is a federal requirement for all tax professionals regardless of the number of clients they serve. The FTC Safeguards Rule doesn’t provide an exemption for small firms or solo practitioners. Every firm that handles sensitive financial data must have a documented plan to protect that information throughout its lifecycle, from acquisition to destruction.

What is a Certificate of Destruction and why do I need one?

A Certificate of Destruction is a formal document provided by a shredding service or generated internally that confirms specific records were permanently destroyed. It serves as an essential part of your audit trail, proving that you followed your documented disposal procedures. If a regulator questions your data handling, this certificate provides the professional evidence needed to demonstrate compliance with federal law.