Would your firm survive a federal fine of $3,500 for every single client record you accidentally tossed in a standard recycling bin? Under the 2026 FACTA Disposal Rule, that’s the reality for tax professionals who fail to implement verified secure document disposal procedures for tax records. It’s understandable if you feel a sense of unease regarding your current retention schedules or the technical difference between clearing and purging digital media. You’ve worked hard to build a legacy of trust, and the fear of an IRS audit or a $10.22 million data breach shouldn’t compromise your professional peace of mind.

We’re here to provide the technical clarity and protective reassurance you need to navigate these high-stakes regulatory waters. This guide will help you master the mandatory standards found in IRS Publication 4557 and the latest NIST SP 800-88 Revision 2 framework. By the end of this article, you’ll have a documented destruction procedure ready to add to your Written Information Security Plan (WISP). This methodical approach ensures your firm remains a disciplined protector of sensitive data while meeting the strict expectations of the FTC Safeguards Rule.

Key Takeaways

- Understand the mandatory requirements of IRS Publication 4557 and how they align with the FTC Safeguards Rule to shield your practice from federal oversight.

- Identify the technical standards for secure document disposal procedures for tax records, including why the DIN 66399 P-4 cross-cut standard is the minimum for financial data.

- Clarify complex retention schedules to determine exactly when sensitive filings and employment tax records should be permanently destroyed.

- Master the protocols for sanitizing digital media and decommissioning old hardware according to the latest NIST SP 800-88 standards.

- Develop a robust framework for documenting your disposal policies within a Written Information Security Plan (WISP) to demonstrate professional accountability.

IRS Publication 4557 and the Legal Mandate for Secure Disposal

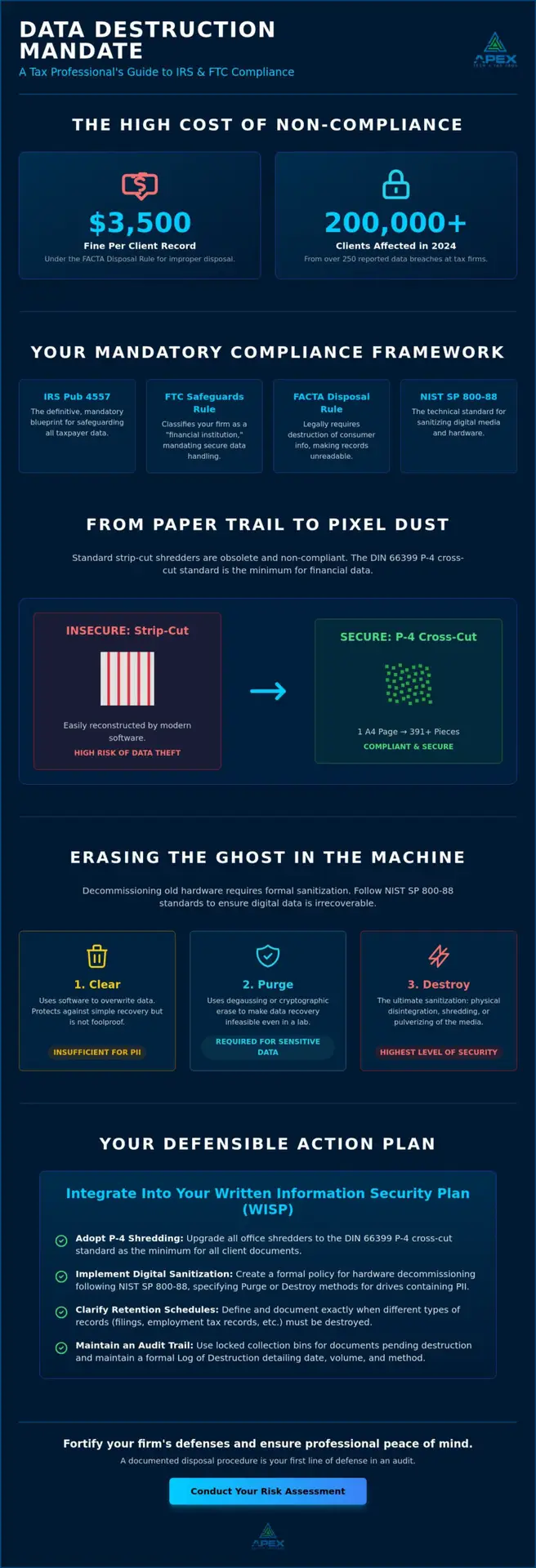

IRS Publication 4557 serves as the definitive blueprint for safeguarding taxpayer data. It isn’t merely a set of best practices; it’s a mandatory standard for all paid tax preparers as of 2026. This publication explicitly requires practitioners to implement secure document disposal procedures for tax records to prevent unauthorized access. When we look at foundational records management principles, the final stage of the record lifecycle is destruction. However, for a tax professional, this stage is fraught with significant regulatory risk. Failure to comply can lead to devastating consequences, including federal fines of up to $3,500 per violation under the FACTA Disposal Rule. Beyond the financial impact, the reputational damage from a publicized data breach often proves fatal for small to mid-sized firms. In 2024 alone, the IRS received over 250 reports of data breaches from tax professionals, affecting over 200,000 clients. To build a legally defensible position, your “reasonable measures” for destruction must be documented and consistently applied within your firm’s operational framework.

The FTC Safeguards Rule Connection

The Federal Trade Commission (FTC) classifies CPA firms and tax preparers as “financial institutions.” This classification subjects your practice to the FTC Safeguards Rule, which includes a specific mandate for the secure disposal of consumer information. You’re required to designate a qualified security coordinator to oversee these processes. This individual ensures that any data used to provide financial services is pulverized, burned, or shredded beyond reconstruction. Consumer information includes any record about an individual that is a “consumer report” or is derived from one. In a tax practice, this covers almost every client file you touch during the engagement. Implementing secure document disposal procedures for tax records is a core component of this federal requirement.

Understanding PII in Tax Records

Personally Identifiable Information (PII) includes more than just Social Security numbers. It encompasses any data that can be used to distinguish or trace an individual’s identity, such as bank account details, prior year adjusted gross income, or even specific filing statuses. Even a partial tax return or a discarded workpaper contains enough PII to facilitate sophisticated identity theft. Modern threats aren’t just digital; “dumpster diving” and social engineering remain active tactics for criminals in 2026. High-security destruction is the only way to ensure that physical records don’t become a liability once they leave your office. If a document is no longer needed, it shouldn’t exist in a readable format. Protecting this data is a mission-driven responsibility that balances technical precision with a commitment to client safety.

Establishing High-Security Destruction Standards for Paper Records

High-security destruction is not a suggestion; it’s an operational requirement for any firm handling sensitive financial data. Many practitioners still rely on outdated strip-cut shredders that merely turn documents into long ribbons. These ribbons are easily reconstructed by modern software and determined adversaries. To implement truly secure document disposal procedures for tax records, firms must adopt cross-cut or micro-cut technology. The global standard for this is DIN 66399. For tax professionals, the P-4 security level is the absolute minimum requirement. This standard ensures that a standard A4 page is rendered into at least 391 pieces, making manual or digital reassembly virtually impossible.

Effective destruction begins long before the paper hits the blades. Your internal policy should mandate the use of locked collection bins for any document containing PII that has reached the end of its lifecycle according to IRS record-keeping requirements. These bins prevent unauthorized access by staff or cleaning crews during the “holding” phase. Maintaining a formal Log of Destruction is also critical. This log should record the date, volume, and method of destruction, providing an audit trail that proves your firm followed its own internal protocols. If you haven’t yet verified your current physical security, conducting a formal risk assessment can identify vulnerabilities in your document lifecycle.

Choosing the Right Shredding Equipment

Security levels are categorized from P-1 to P-7. While P-4 is the baseline for financial records, P-5 and P-6 provide even smaller particle sizes for highly sensitive corporate tax data. P-7 is typically reserved for top-secret government intelligence. Avoid strip-cut shredders entirely. They are a compliance risk because they leave data legible. If shredding in-house, ensure your equipment is oiled regularly. Dull blades produce larger, less secure fragments that may no longer meet P-4 specifications.

Working with Third-Party Disposal Vendors

Professional shredding services offer a scalable solution, but they require rigorous vetting. Ensure your vendor holds a National Association for Information Destruction (NAID) certification. This certification confirms they follow strict security protocols, including background-checked personnel and a secure chain of custody. Under the FTC Safeguards Rule, you must have a written contract that requires the service provider to maintain appropriate safeguards. Always demand a “Certificate of Destruction” after each service. This document serves as primary evidence for IRS auditors that you have followed secure document disposal procedures for tax records.

Tax Record Retention Schedules: Knowing When to Dispose

Many professionals mistakenly view an ever-growing archive as a safety net. In reality, an overstuffed filing cabinet or a bloated server is a significant liability. Every record your firm retains is a record you’re legally obligated to protect. If you haven’t established clear secure document disposal procedures for tax records, you’re essentially maintaining a larger target for potential data breaches. A disciplined annual purge isn’t just about reclaiming office space; it’s a critical security function that limits your firm’s exposure to IRS and FTC scrutiny.

The general rule for individual tax returns is a three-year retention period from the date of filing or the due date, whichever is later. This period represents the standard statute of limitations for the IRS to assess additional tax. However, this window is not universal. If a taxpayer understates their gross income by more than 25%, the statute of limitations extends to six years. For claims involving bad debt or worthless securities, you must maintain records for seven years. Employment tax records require a different approach, with a mandatory minimum retention of four years after the tax becomes due or is paid.

IRS Statutes of Limitations

While the three-year rule covers most scenarios, certain situations demand indefinite retention. There’s no statute of limitations for fraudulent returns or for years when no return was filed. In these high-stakes cases, your firm must be prepared to defend the taxpayer’s history regardless of how much time has passed. This nuance highlights why a “one size fits all” destruction policy is insufficient for a sophisticated practice. You need a nuanced inventory system that flags specific files for destruction based on their unique risk profiles and filing histories.

Permanent Records vs. Disposable Data

Certain documents should never enter your destruction cycle. Corporate charters, minutes, bylaws, and property records with long-term tax basis implications must be kept permanently. It’s equally important to distinguish between firm-generated workpapers and client-provided originals. According to the FTC’s Disposal Rule, you’re responsible for the secure destruction of any consumer information derived from credit reports or background checks. We recommend clearly outlining your secure document disposal procedures for tax records in your annual engagement letters. This transparency ensures clients understand when their data will be purged and encourages them to maintain their own primary copies, further reducing your firm’s role as a perpetual data steward.

Establishing a fixed date for your annual purge, such as the mid-June lull, helps transform compliance from a frantic reaction into a methodical process. This steady, deliberate rhythm mirrors the meticulous nature of the profession you serve and ensures that your firm’s data footprint remains lean and defensible.

Beyond the Shredder: Secure Disposal of Digital Tax Data and Hardware

While physical shredding is a visible act of protection, the digital lifecycle of tax data presents a more complex challenge. Simply dragging a file to the “Trash” or formatting a drive does not constitute disposal. These actions merely remove the pointers to the data, leaving the sensitive PII intact and recoverable by even basic forensic tools. To remain compliant with federal standards, your firm’s secure document disposal procedures for tax records must account for the persistent nature of electronic media. This includes every device that has ever touched client data, from primary servers to the internal hard drives of office copiers.

Office copiers and all-in-one printers are often the silent vulnerabilities in a tax practice. These devices contain internal caches and hard drives that store images of every document scanned, printed, or faxed. When you return a leased machine or sell an old unit, that unencrypted data remains. Modern protocols require a verified wipe or physical destruction of these internal drives. For cloud-based storage, the responsibility remains with the practitioner to ensure the provider adheres to NIST standards for data sanitization. If you’re unsure where your data currently resides or how it’s being retired, a comprehensive risk assessment can help map your digital footprint and identify these hidden exposure points.

Digital Sanitization Methods

The gold standard for media sanitization in 2026 is NIST SP 800-88 Revision 2. This framework, finalized in late 2025, defines three levels of data destruction: Clear, Purge, and Destroy. “Clear” applies basic software-based overwriting, while “Purge” uses more advanced techniques like cryptographic erasure to make data recovery infeasible even in a laboratory setting. For high-impact tax data, physical destruction of the drive remains the most definitive “Destroy” method. When managing end-of-life for encrypted cloud backups, you must verify that the encryption keys are permanently deleted, effectively rendering the data unreadable.

Mobile Device and Tablet Decommissioning

Mobile devices require a specialized approach due to their integrated flash storage. A standard factory reset is often insufficient for professional compliance. Instead, practitioners should utilize cryptographic erasure, which destroys the internal encryption keys. Before any device leaves your control, ensure all firm-managed accounts are removed via your Mobile Device Management (MDM) software. Every decommissioned asset should be logged by its serial number in your firm’s records. This documentation proves that your secure document disposal procedures for tax records extend to the hardware level, providing a mission-driven defense against potential audits.

Integrating Disposal Procedures into Your Written Information Security Plan (WISP)

A Written Information Security Plan (WISP) serves as the structural foundation of your firm’s compliance program. Many practitioners mistakenly treat this as a static document focused solely on firewalls and passwords. This narrow focus creates a dangerous regulatory gap. Under IRS Publication 4557, your WISP must explicitly detail how you handle the end of the data lifecycle. Without formal secure document disposal procedures for tax records, your WISP is essentially incomplete. This omission leaves your practice vulnerable to claims of negligence during an FTC or IRS inquiry. Documentation is the only evidence that your physical and digital destruction acts are part of a disciplined, professional process.

Compliance is not a one-time event but a continuous culture within your firm. Because 74% of all data breaches involve a human element, such as improper handling of sensitive files, your disposal protocols must be reinforced through Cybersecurity Awareness Training. Staff members need to know exactly which bin to use and which digital files require cryptographic erasure. Regularly reviewing these procedures ensures that as your technology stack evolves, your security remains airtight. A methodical approach to documentation signals to both clients and regulators that their sensitive data is in safe, capable hands.

Drafting Your Disposal Policy

Your policy must define specific roles to ensure accountability. Clearly state who in the firm is authorized to approve data destruction and oversee the chain of custody. You should also establish a fixed frequency for these actions, such as monthly shredding cycles or quarterly digital purges. A well-drafted policy sentence for your WISP might read: “Our firm mandates that all physical records containing PII be destroyed via P-4 cross-cut shredding and all digital media be sanitized according to NIST SP 800-88 Purge standards prior to hardware decommissioning or file disposal.”

The Role of Professional Risk Assessments

A professional risk assessment is the most effective way to identify hidden gaps in your current disposal workflow. It bridges the gap between your digital IT security and the physical security of your office space. For example, an assessment might reveal that while your servers are secure, your “to be shredded” bin is accessible to unauthorized personnel. Integrating these findings into your WISP transforms it from a generic template into a customized shield for your practice. You can download our FREE WISP Template to start documenting your disposal procedures today and ensure your firm meets the 2026 standards for professional accountability.

Protecting Your Legacy Through Disciplined Data Destruction

Establishing secure document disposal procedures for tax records is a mission-critical responsibility that extends far beyond the physical shredder. By aligning your firm’s operations with the P-4 paper standards and NIST 800-88 digital sanitization protocols, you’ve taken the first step toward mitigating the risk of a devastating breach. However, true security is only achieved when these technical standards are integrated into a documented, living framework. Your firm’s heritage and client trust are too valuable to leave to chance or unwritten policies.

We provide the specialized expertise needed to bridge the gap between regulatory theory and daily practice. From expert-led Risk Assessments that identify hidden vulnerabilities to specialized cybersecurity training for tax staff, our approach is engineered for the unique demands of your profession. Let us help you transform your security posture into a position of strength. You can Get a Customized WISP and Secure Your Firm using our IRS Publication 4557 compliant frameworks. Taking this step ensures that your sensitive data remains in safe, capable hands while you focus on the continued success of your clients. Your commitment to compliance is the ultimate safeguard for your practice’s future.

Frequently Asked Questions

What is the IRS standard for document shredding?

The IRS requires that all sensitive taxpayer data be rendered unreadable and undecipherable to prevent unauthorized access. While they don’t mandate a specific brand of equipment, professional standards dictate the use of cross-cut or micro-cut shredders that meet the DIN 66399 P-4 security level. This technical standard ensures that any document containing Personally Identifiable Information (PII) is destroyed beyond any possibility of reconstruction, protecting your firm from potential liability.

How long must a tax professional keep client records before disposal?

Most individual tax records should be retained for three years from the date of filing or the due date. However, this period extends to six years for substantially underreported income and seven years for claims of bad debt or worthless securities. Employment tax records must be kept for at least four years. Maintaining a disciplined inventory system ensures you don’t keep data longer than necessary, which reduces your firm’s overall risk profile.

Do I need a certificate of destruction for tax records?

A Certificate of Destruction is a critical piece of evidence for your compliance audit trail. If you utilize a third-party vendor, this document proves that your secure document disposal procedures for tax records were followed correctly. It verifies the date, method, and chain of custody, providing a mission-driven defense during an IRS or FTC inquiry. Without this documentation, you lack the professional proof needed to demonstrate adherence to federal disposal mandates.

Is it better to shred tax documents in-house or hire a service?

The choice depends on your firm’s volume and capacity for internal oversight. In-house shredding requires high-end P-4 equipment and dedicated staff time, while professional NAID-certified services offer a secure, documented chain of custody. Many firms prefer third-party services because they provide the necessary documentation to satisfy the FTC Safeguards Rule without the operational burden of equipment maintenance. Both methods are valid if they meet the required technical standards for data destruction.

How do I securely dispose of an old computer used for tax prep?

Securely retiring a computer requires following NIST SP 800-88 standards for media sanitization. Simply deleting files or formatting the drive is insufficient because data remains recoverable. You should perform a cryptographic erasure to destroy the internal encryption keys or physically destroy the hard drive. This methodical approach ensures that no residual client data remains on the hardware before it leaves your firm’s control, maintaining your commitment to client confidentiality.

What happens if I dispose of tax records prematurely?

Premature disposal can lead to the IRS disallowing deductions or credits during an audit because you lack the necessary supporting evidence. Beyond tax adjustments, early destruction can trigger penalties under the FTC Safeguards Rule if it contradicts your documented retention policy. It’s essential to follow your firm’s established schedule to maintain professional accountability. Keeping records for the correct duration is just as important as the method you use for their eventual destruction.

Does the FTC Safeguards Rule apply to small, solo tax practices?

The FTC Safeguards Rule applies to all tax preparers regardless of their firm’s size. Solo practitioners are classified as “financial institutions” under federal law and must maintain a Written Information Security Plan (WISP). Small practices aren’t exempt from the technical standards for data protection or the requirement to implement secure document disposal procedures for tax records. Every practitioner carries the same legal weight when it comes to protecting sensitive taxpayer information.

How do I document document disposal in my WISP?

Your WISP should include a specific section titled “Data Destruction and Disposal” that outlines your administrative and technical safeguards. This section must define who is authorized to destroy data, the specific security levels used for destruction, and the frequency of your disposal cycles. Documenting these steps transforms your daily actions into a legally recognized compliance framework. It provides the protective reassurance that your firm operates with the clinical precision required in high-stakes environments.