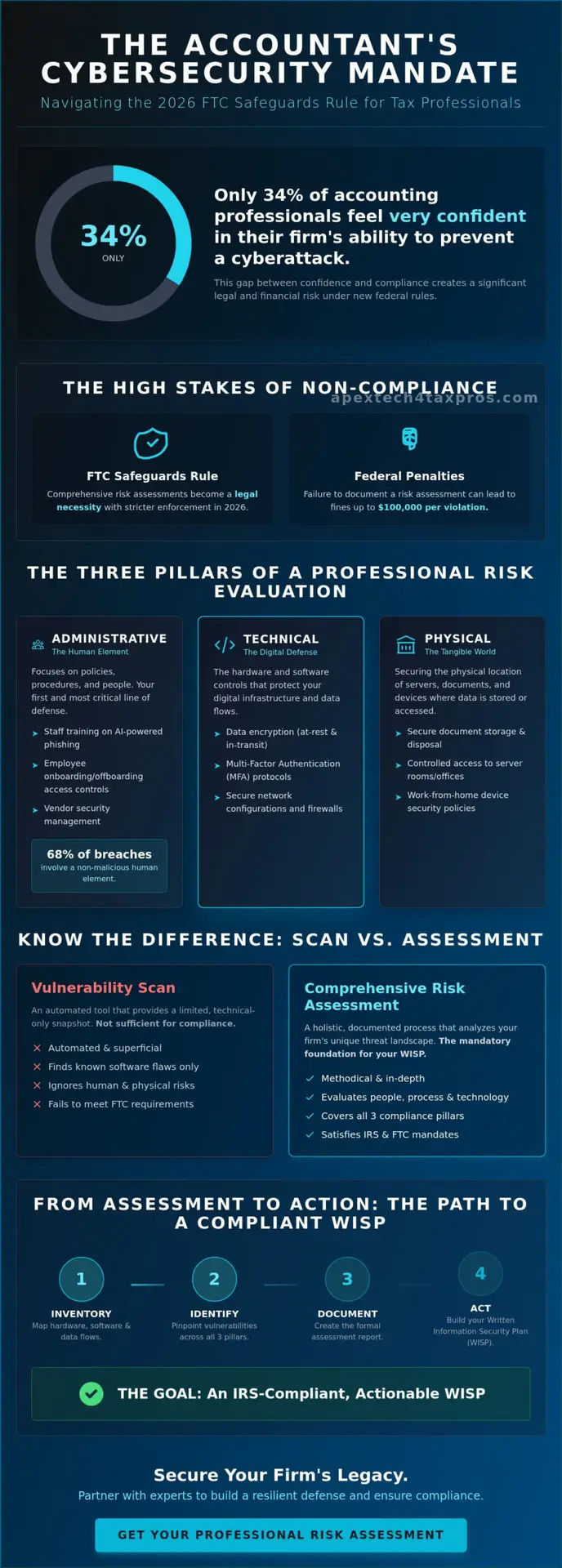

Did you know that only 34 percent of accounting professionals feel very confident in their firm’s ability to prevent a cyberattack? This statistic highlights a troubling gap between federal expectations and firm reality. As 2026 brings stricter enforcement of the FTC Safeguards Rule, performing a comprehensive cybersecurity risk assessment for accounting firms is no longer a technical suggestion; it’s a legal necessity. We understand that the pressure to protect client PTINs and sensitive financial data while managing a practice can feel overwhelming, especially when federal fines for non-compliance can reach $100,000 per violation.

You likely recognize that a simple software scan isn’t the same as a full risk assessment, yet the distinction often feels blurred by complex jargon. This guide simplifies that process, promising to show you how to conduct a professional assessment that satisfies IRS Publication 4557 mandates and builds a resilient defense against AI-powered phishing. We’ll walk through the specific technical controls required by the FTC, the role of a designated Qualified Individual, and how to turn these requirements into a repeatable annual security process. By the end, you’ll have the clarity needed to secure your firm’s legacy and ensure your client data remains in safe, capable hands.

Key Takeaways

- Understand why a professional cybersecurity risk assessment for accounting firms is the mandatory foundation for satisfying the FTC Safeguards Rule in 2026.

- Learn to evaluate your firm through the lens of administrative and technical safeguards, ensuring your encryption and MFA protocols meet federal standards.

- Discover the critical distinction between automated vulnerability scans and a holistic risk assessment that identifies how and where your sensitive data actually flows.

- Follow a structured framework to inventory your hardware and software, creating a clear map of taxpayer data from initial intake to final e-filing.

- Master the transition from assessment to action by using your findings to build a customized Written Information Security Plan (WISP) that meets IRS expectations.

What is a Cybersecurity Risk Assessment for Accounting Firms?

A cybersecurity risk assessment for accounting firms is a methodical, documented evaluation of how your practice collects, stores, and transmits taxpayer data. It isn’t a one-time software installation or a simple antivirus scan. Instead, it’s a diagnostic process that identifies vulnerabilities before they become liabilities. While “security” refers to the current state of your defenses, the “assessment” is the active investigation that determines if those defenses are actually working. This comprehensive evaluation serves as the mandatory foundation for an IRS-compliant Written Information Security Plan (WISP).

Under the Gramm-Leach-Bliley Act (GLBA), accounting firms are classified as financial institutions. This classification triggers the FTC Safeguards Rule, making these assessments non-negotiable for 2026. The shift from best practice to federal mandate is clear; the government now requires proof that you’ve analyzed your firm’s specific threat landscape. Failure to document this process can lead to fines of up to $100,000 per violation, a risk that no professional practice should ignore.

The IRS Publication 4557 Connection

IRS Publication 4557 outlines the specific standards tax professionals must meet to protect taxpayer data. The IRS uses these assessments to verify that a firm has implemented “reasonable” security measures. When you renew your PTIN or tax software each year, you’re often confirming that you have a WISP in place. You can’t legally have a WISP without first conducting a risk assessment to identify what you’re actually protecting. Federal guidelines focus on several core areas:

- Management and educational safeguards for staff

- Information systems and software integrity

- Physical office security and document disposal

- External threats like AI-powered phishing

The FTC Safeguards Rule Requirements

The FTC Safeguards Rule requires firms to identify “reasonably foreseeable” internal and external risks that could result in the unauthorized disclosure of client information. This isn’t just about hackers; it’s about evaluating staff training, physical office security, and vendor management. You must also designate a Qualified Individual to oversee this evaluation. This person is responsible for ensuring the assessment isn’t a check-the-box exercise but a genuine analysis of your firm’s unique environment. Many firms align their process with the NIST Cybersecurity Framework to ensure their methodology meets global standards for data protection. Since 2024, the FTC also requires notification of breaches involving at least 500 consumers within 30 days, making your initial risk assessment the most important tool for preventing such a crisis.

The Three Pillars of a Professional Accounting Risk Evaluation

A professional cybersecurity risk assessment for accounting firms rests on three distinct pillars: administrative, technical, and physical safeguards. Relying solely on software is a common pitfall that leaves firms vulnerable during regulatory reviews. Federal auditors look for a holistic approach that proves you’ve considered every possible path a bad actor might take to reach sensitive data. If your security strategy stops at your firewall, you aren’t just risking a breach; you’re failing to meet the “reasonable” standard required by federal law.

Administrative Risks: The Human Element

According to the 2024 Verizon Data Breach Investigations Report, 68 percent of data breaches involved a human element. This makes staff training your first line of defense. In 2026, AI-powered phishing attacks have become so sophisticated that even seasoned partners can be deceived. Your assessment must evaluate how you train seasonal employees and whether your onboarding procedures include immediate access revocation upon departure. This documentation is a key requirement of IRS Publication 4557, which mandates that your security plan be active and managed rather than a static document.

Technical Risks: Beyond the Firewall

Modern compliance requires more than just a firewall. You need to analyze how data is encrypted while it’s sitting on your server and while it’s being sent to a client. Traditional email attachments are no longer considered a secure safeguard for tax documents. Instead, your assessment should verify the integrity of your client portals and the immutability of your cloud backups. If your backup isn’t protected by an “air-gap” or a similar immutable protocol, a single ransomware event could wipe out years of records. For firms looking to strengthen these defenses, implementing customized risk assessments can identify these technical gaps before they are exploited.

Physical safeguards are the third, often overlooked, pillar. Performing a thorough cybersecurity risk assessment for accounting firms ensures that your physical office security matches your digital strength. This includes:

- Reviewing clean-desk policies to ensure sensitive taxpayer data isn’t left in plain sight.

- Assessing office access controls for visitors and cleaning crews.

- Documenting a secure process for the physical destruction of hard drives and old hardware.

Simply deleting files isn’t enough; the FTC Safeguards Rule expects a documented process for hardware disposal. If an unencrypted laptop is stolen or a retired copier is sold with its hard drive intact, the resulting breach notification requirements are the same as a digital hack. A truly professional evaluation treats your office door and your server room with the same level of vigilance.

Vulnerability Scanning vs. Comprehensive Risk Assessment

Many firm owners receive a technical PDF from an automated tool and believe their federal compliance requirements are met. This is a dangerous misconception that can lead to significant audit findings. A vulnerability scan is essentially a digital health check that looks for unpatched software or open ports. It identifies the “what” in your system. However, a cybersecurity risk assessment for accounting firms is a holistic process that examines the “why” and “how” of your data protection. It bridges the gap between raw technical data and your actual business operations.

Context is the defining factor in professional risk management. An automated scan might flag an old printer with severe security flaws as a critical threat. If that printer isn’t connected to your network and only handles non-sensitive internal memos; the actual risk to your client data is negligible. Conversely, a scan might show a “secure” cloud portal as perfectly safe. A risk assessment would reveal that your staff shares a single login password on a sticky note. No software scan can detect that massive vulnerability. It requires a human professional to evaluate the intersection of technology and firm behavior.

When a Simple Scan is Sufficient

Automated scans aren’t useless; they are vital for routine IT maintenance. They are perfect for quarterly health checks that help your team identify immediate patch requirements for tax preparation software. They also validate that your firewall remains active and correctly configured after a major system update. Think of these scans as a maintenance tactic rather than a compliance strategy. They ensure your technical foundations remain solid between your more rigorous annual evaluations.

Why the IRS Mandates a Full Assessment

The IRS and FTC require more than just a list of software patches. They demand documentation of “compensating controls.” These are the manual processes or secondary defenses that protect data when a primary technical control isn’t feasible. A thorough cybersecurity risk assessment for accounting firms also evaluates your third-party SaaS providers. It ensures that your cloud-based tax software and document storage meet the same rigorous standards as your internal systems. Professionals often utilize the AICPA’s SOC for Cybersecurity framework to structure this evaluation. This methodology helps you create the “Impact vs. Likelihood” matrix required for a professional WISP. By weighing the probability of a threat against its potential damage, you can prioritize your security budget where it’s needed most.

A Step-by-Step Framework for Conducting Your Annual Assessment

Conducting a cybersecurity risk assessment for accounting firms requires a methodical approach that mirrors the precision of a tax audit. It’s a disciplined process that moves from high-level discovery to granular remediation. By following a structured framework, you ensure that no digital corner of your practice remains unexamined. This systematic evaluation isn’t just about finding flaws; it’s about building a defensible record of your firm’s commitment to taxpayer data protection. A professional assessment typically follows five essential stages:

- Step 1: Inventory. Catalog every piece of hardware and every software application that touches taxpayer data.

- Step 2: Data Mapping. Trace the lifecycle of sensitive information from initial client intake through to final e-filing.

- Step 3: Threat Identification. Analyze the likelihood of specific events like ransomware, insider threats, or the physical loss of a mobile device.

- Step 4: Control Evaluation. Compare your current safeguards against federal requirements to identify the “Gap” in your defenses.

- Step 5: Prioritization. Create a remediation roadmap based on your firm’s specific risk appetite and regulatory deadlines.

Inventory Management for Tax Pros

Your registry must include more than just the servers in your office. It needs to account for mobile devices, home-office laptops, and even the personal tablets used by seasonal staff. You must also identify and purge “shadow IT” applications, such as unapproved cloud storage or personal messaging apps used to communicate with clients. You cannot protect what you have not documented. If you’re unsure where to start with your hardware registry, our team provides professional risk assessments to identify these hidden gaps for you.

Mapping the Tax Data Lifecycle

Understanding how a W-2 moves from a client’s hand to your secure storage is critical for a successful cybersecurity risk assessment for accounting firms. You need to identify “choke points” where data might be unencrypted, such as during the transition from a physical scanner to a local network folder. Don’t forget to evaluate the security of the “last mile,” which is how the client receives their finished return. If you’re still sending password-protected PDFs via standard email, your data mapping will likely reveal a significant compliance vulnerability that requires immediate attention. This lifecycle analysis ensures that your security measures stay attached to the data, regardless of where it resides in your workflow.

From Assessment to Action: Building Your IRS-Compliant WISP

A cybersecurity risk assessment for accounting firms isn’t just a discovery tool; it’s the legal evidence that justifies every policy in your Written Information Security Plan (WISP). The IRS and FTC don’t just want to see a binder on a shelf. They require a living document that’s tailored to the specific vulnerabilities found during your evaluation. If your WISP claims you use Multi-Factor Authentication but your assessment shows your legacy tax software doesn’t support it, you have a documented contradiction that auditors will quickly identify. Your assessment provides the factual “why” behind your security “how.”

Turning identified gaps into a prioritized remediation plan is the final step in achieving 2026 compliance. This plan serves as your roadmap for technical and administrative upgrades, allowing you to demonstrate to governing bodies that you’re actively working to mitigate risks. Apex Tech 4 Tax Pros bridges the gap between evaluation and execution, ensuring that your firm doesn’t just identify problems but solves them through engineered, industry-specific solutions. We help you move from a state of vulnerability to a state of secure, documented compliance.

The Dangers of Using Generic WISP Templates

Using a boilerplate template without a preceding risk assessment is a significant red flag for IRS auditors. A generic document can’t account for your firm’s specific hardware inventory or the unique way your staff handles sensitive client data. While a generic template might offer a basic outline of security protocols, it lacks the empirical data required to prove that your firm has actually evaluated its own unique environment. The FTC Safeguards Rule requires you to designate a “Qualified Individual” to oversee your program, and a template can’t fulfill this role. It requires a designated professional who understands your firm’s technical infrastructure. Professional assessments provide the “Reasonable Basis” required by the FTC, proving that your security measures are grounded in actual data rather than guesswork.

Next Steps for Your Firm

The most effective time to address these requirements is before the peak tax season rush begins. Scheduling your annual assessment early ensures that your defenses are hardened before the volume of sensitive data increases. Once the assessment is complete, integrate the findings into your monthly staff security training to keep your team vigilant against evolving digital threats. Secure your practice today with a professional risk assessment and customized WISP to ensure your firm is protected and compliant for the upcoming year. Taking action now protects your client PTINs and secures your firm’s professional legacy.

Securing Your Firm’s Future in a Regulated Landscape

The path toward 2026 compliance requires a transition from reactive software scans to proactive, methodical evaluations. You’ve seen how a comprehensive cybersecurity risk assessment for accounting firms serves as the vital evidentiary link between your daily operations and your mandatory Written Information Security Plan (WISP). By addressing the administrative, technical, and physical pillars of your practice, you don’t just satisfy the FTC Safeguards Rule; you build a resilient culture that protects your clients’ most sensitive financial data.

Generic templates cannot replace the precision of an expert-led evaluation tailored to the high-stakes environment of tax preparation. At Apex Tech 4 Tax Pros, we specialize in bridging the gap between complex IRS Publication 4557 requirements and your firm’s specific technical infrastructure. Our customized security plans are engineered specifically for tax professionals, ensuring your practice remains both secure and fully compliant. We identify critical vulnerabilities and provide the professional remedy needed to meet federal standards.

Don’t let regulatory burdens distract you from your core mission of serving clients. Get Your Professional Risk Assessment & IRS-Compliant WISP today to secure your firm’s legacy. With a repeatable annual process in place, you can enter the next tax season with the confidence that your data is in safe, capable hands.

Frequently Asked Questions

Is a cybersecurity risk assessment required by the IRS?

Yes, the IRS requires a cybersecurity risk assessment for accounting firms as a foundational component of Publication 4557 compliance. This mandate is reinforced by the FTC Safeguards Rule, which classifies tax preparers as financial institutions. You must document your evaluation of internal and external risks to taxpayer data to maintain your EFIN and demonstrate that you’ve implemented “reasonable” security measures during a federal audit.

How often should an accounting firm perform a risk assessment?

You should perform a formal risk assessment at least once per year. Federal guidelines also require an updated evaluation whenever there is a material change to your firm’s operations. This includes adopting new tax preparation software, moving to a different physical office, or experiencing significant changes in your staffing levels. Regular reviews ensure your security posture remains effective against evolving threats like AI-powered phishing.

What is the difference between a risk assessment and a WISP?

A risk assessment is the diagnostic process used to identify specific vulnerabilities, while a Written Information Security Plan (WISP) is the formal policy document that outlines how you will address those risks. Think of the assessment as the evidence that justifies your security choices. The IRS requires your WISP to be specifically tailored based on the findings of your individual risk assessment rather than being a generic template.

Can I perform my own cybersecurity risk assessment as a solo practitioner?

While solo practitioners can technically perform their own assessments, the FTC Safeguards Rule requires the designation of a “Qualified Individual” to oversee the process. Most small firms find it difficult to maintain the objective technical expertise required to identify subtle network vulnerabilities. Utilizing a professional service ensures your documentation meets the rigorous standards expected by federal auditors and provides a level of professional accountability that self-assessments often lack.

What are the penalties for not having a documented risk assessment?

Non-compliance can result in severe financial and professional consequences. The FTC can levy fines of up to $100,000 per violation, and the civil penalty for violating the FTC Act can reach $51,744 per day. Beyond monetary losses, the IRS may revoke a preparer’s Electronic Filing Identification Number (EFIN), effectively halting your ability to conduct business during the critical tax season.

Does my professional liability insurance require a risk assessment?

Many professional liability insurance carriers now require proof of a documented risk assessment and a WISP as a condition for coverage or renewal. Carriers view these documents as evidence of proactive risk management. Failing to maintain these records can lead to increased premiums or a total denial of coverage in the event of a data breach, leaving your practice financially exposed to client litigation.

What should be included in a risk assessment report for accountants?

A comprehensive report must include a full inventory of all hardware and software that touches taxpayer data. It should also feature a detailed map of your data lifecycle, an identification of specific threats like ransomware, and an evaluation of your existing administrative and technical safeguards. Finally, the report must conclude with a prioritized remediation plan that addresses any identified gaps in your firm’s security posture.

How long does a professional cybersecurity risk assessment take to complete?

The duration of a cybersecurity risk assessment for accounting firms typically ranges from two to four weeks depending on the complexity of your technical infrastructure. This timeline includes the initial discovery phase, technical testing, and the production of the final report. Starting the process well before the peak tax season ensures you have ample time to implement any required remediation steps without disrupting your client service.