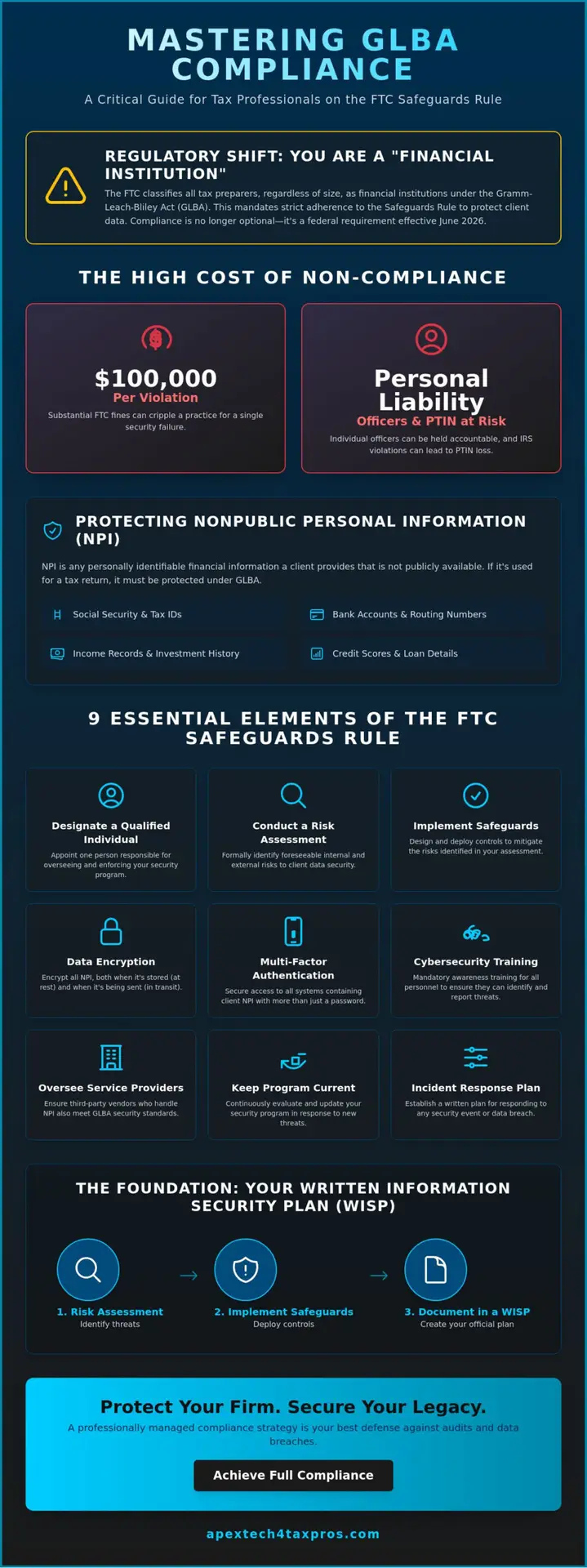

Could a federal audit or a single security oversight dismantle the legacy you’ve spent decades building? As of June 2026, the regulatory environment has shifted from general guidelines to prescriptive mandates, making glba compliance for tax preparers a non-negotiable pillar of professional practice. The FTC Safeguards Rule now requires specific technical controls, including mandatory encryption for data at rest and in transit, alongside the designation of a Qualified Individual to oversee your security program. The stakes are high, as financial institutions can face fines up to $100,000 per violation, and individual officers may be held personally accountable for failures in oversight.

It’s understandable if the complexity of these federal regulations feels overwhelming, especially when you’re focused on delivering results for your clients. You’ve worked hard to earn their trust, and the fear of a data breach or a failed audit is a heavy burden to carry. This definitive guide will help you master the complexities of the Gramm-Leach-Bliley Act and the FTC Safeguards Rule, ensuring you meet every mandatory standard with confidence. We’ll examine the specific requirements for a defensible Written Information Security Plan (WISP), clarify the role of the Qualified Individual, and outline the technical safeguards needed to shield your firm from federal fines and catastrophic data loss.

Key Takeaways

- Understand why the FTC classifies all tax professionals as financial institutions, mandating strict adherence to the Gramm-Leach-Bliley Act regardless of practice size.

- Identify the nine essential elements of the FTC Safeguards Rule, focusing on mandatory technical controls like multi-factor authentication and data encryption.

- Learn how to conduct a formal risk assessment to identify foreseeable internal and external threats, providing the necessary foundation for your Written Information Security Plan (WISP).

- Secure your practice by designating a Qualified Individual and implementing mandatory cybersecurity awareness training to ensure glba compliance for tax preparers.

- Discover how a professionally managed compliance strategy acts as a defensive shield during IRS or FTC inquiries while reinforcing the trust your clients place in your firm.

Understanding the GLBA Mandate for Tax Professionals

The Gramm-Leach-Bliley Act (GLBA) serves as the foundational pillar for consumer financial privacy in the United States. While the law was enacted in 1999, its scope has expanded through rigorous updates to the FTC Safeguards Rule. Many practitioners are surprised to learn that the Federal Trade Commission classifies even solo tax preparers as “financial institutions.” This isn’t an exaggeration or a clerical error. If you’re significantly engaged in providing financial products or services, you’re subject to the same rigorous data protection standards as a regional bank. Establishing glba compliance for tax preparers is a mission-critical objective that protects both your clients’ identities and the professional standing of your firm.

The regulatory landscape in 2026 reflects a shift toward zero-tolerance for security negligence. Recent FTC enforcement trends show a move away from simple warnings toward substantial financial penalties and mandatory audits. The primary goal of these regulations is the protection of Nonpublic Personal Information (NPI). By securing this data, you don’t just satisfy a federal requirement; you insulate your practice from the reputational ruin that follows a data breach.

The Definition of Nonpublic Personal Information (NPI)

NPI includes any “personally identifiable financial information” that a client provides to you to receive tax services. It’s information that isn’t otherwise available through public records. Under the GLBA, there’s a “reasonable expectation of privacy” for any data collected during the tax preparation process. This includes:

- Social Security numbers and tax identification numbers.

- Bank account details, routing numbers, and income records.

- Credit scores and loan application details.

- Investment history and retirement account balances.

If you’ve collected a piece of data to complete a Form 1040 or a corporate return, it’s almost certainly protected NPI. Distinguishing between public data, like property tax assessments, and protected NPI is vital for determining which records require the highest level of encryption and access control.

Why Tax Preparers Face Stricter Scrutiny

Tax professionals are prime targets for cybercriminals because tax data is incredibly valuable on the dark web. A single tax return contains everything a bad actor needs to commit comprehensive identity theft. This high risk is why glba compliance for tax preparers is scrutinized so heavily by both the FTC and the IRS.

There’s a significant overlap between the FTC Safeguards Rule and IRS Publication 4557, “Safeguarding Taxpayer Data.” While the FTC focuses on the broad financial institution mandate, the IRS links these security standards directly to your ability to practice. Failing to meet these standards can result in the loss of your Preparer Tax Identification Number (PTIN) and significant federal fines. We’ve seen that a robust security posture isn’t just about avoiding a $100,000 penalty; it’s about preserving the legacy of your practice and the trust of the families you serve.

The FTC Safeguards Rule: Core Technical Requirements

The transition from “best practices” to “mandatory requirements” is now absolute. Under 16 CFR Part 314, the FTC outlines nine specific elements that every information security program must include to be legally defensible. While the rule offers some scalability, firms with 5,000 or more consumers face the most prescriptive requirements, including written risk assessments and annual board reporting. Regardless of your firm’s size, achieving glba compliance for tax preparers involves moving beyond simple password protection toward a multi-layered technical defense system. This framework is designed to ensure that the complexity of your controls matches the volume and sensitivity of the data you manage.

The AICPA resources provide a helpful starting point for understanding how these federal mandates translate into daily accounting workflows. Implementing these standards isn’t just about ticking boxes for a regulator; it’s about building a resilient infrastructure that protects your firm’s most valuable asset: client trust. If you aren’t sure where your current system stands, starting with a professional risk assessment can help identify the gaps in your technical safeguards before they become liabilities.

Access Controls and Multi-Factor Authentication (MFA)

The Safeguards Rule explicitly requires firms to implement technical access controls that limit information to only those who need it. This is often referred to as the principle of “least privilege.” In a tax office, this means an administrative assistant shouldn’t have the same system-wide permissions as a senior partner. Multi-factor authentication serves as the single most effective barrier against credential theft by requiring a second form of verification beyond a simple password. In 2026, MFA is no longer a suggestion; it’s a mandatory requirement for any individual accessing systems that contain customer information.

Encryption and Secure Data Disposal

Data protection must be constant, whether information is sitting on a server or moving across the internet. The rule requires all Nonpublic Personal Information (NPI) to be encrypted both at rest and in transit. This means your email communications, cloud storage, and local backups must use high-level encryption standards to remain compliant. Secure disposal is equally critical. You must have a defined process for the permanent destruction of digital records and the shredding of physical documents once they’re no longer required. Shadow IT, such as using personal email accounts or unapproved cloud storage to handle client documents, creates significant vulnerabilities that the Safeguards Rule specifically aims to eliminate.

Conducting a Mandatory Risk Assessment: The Foundation of Your WISP

A Written Information Security Plan (WISP) is legally insufficient if it isn’t preceded by a formal risk assessment. The FTC Safeguards Rule mandates that your plan must be tailored to the specific risks your firm faces. This is where many practitioners falter; they download a template and assume they’ve achieved glba compliance for tax preparers. However, a generic document doesn’t account for your unique technical environment or the specific ways you handle nonpublic personal information (NPI). A defensible security posture begins with a meticulous evaluation of “reasonably foreseeable” internal and external risks. This process ensures that your protective measures are engineered for your specific operational reality rather than a generic industry average.

In 2026, the definition of foreseeable risk has evolved to include AI-driven phishing attacks and sophisticated ransomware strains that can bypass traditional antivirus software. You can find comprehensive AICPA guidance on GLBA compliance to help structure this process. Your assessment must inventory every data asset, from cloud storage buckets to the physical servers in your office, while identifying every software vulnerability that could serve as an entry point for an intruder. This inventory serves as the baseline for your security program, allowing you to track and protect every piece of hardware and software that touches client data.

Step-by-Step Risk Identification

Effective risk identification requires a multi-disciplinary approach. Start with physical security by evaluating who has access to your office and whether paper files are stored in locked, fireproof cabinets. Digital vulnerabilities require a deeper dive into your network infrastructure; check for outdated firmware, the presence of robust firewalls, and the security protocols of your office Wi-Fi. Finally, analyze the human element. Your staff is your first line of defense, yet they’re often the most vulnerable. Assess their susceptibility to social engineering and identify where a lack of clear security policies might lead to accidental data exposure or credential theft.

Mapping Safeguards to Identified Risks

Once you’ve identified your vulnerabilities, you must map specific safeguards to each risk. This customization is what transforms a generic template into a compliant WISP. Prioritize high-impact threats like unauthorized remote access and ransomware that could halt your operations during peak tax season. It’s vital to document the rationale behind your chosen controls. If you choose a specific encryption method or a particular secure cloud backup solution, your WISP should explain how that choice directly mitigates a risk identified during your assessment. Remember that your WISP isn’t a static document; it’s a living framework that must evolve as your firm grows and new cyber threats emerge.

The Human Element: Personnel Training and Third-Party Oversight

Technical safeguards provide the shield, but your personnel are the ones who hold it. The FTC Safeguards Rule recognizes that even the most robust encryption can be bypassed by a single misplaced click or a compromised password. This is why human-centric policies are a core requirement for glba compliance for tax preparers. In 2026, the regulatory expectation has moved toward continuous monitoring, requiring firms to ensure that staff aren’t just trained once, but are consistently adhering to established security protocols. This creates a culture of vigilance that protects your firm’s legacy from the inside out.

The human element of your security program must be as disciplined as your technical infrastructure. By integrating clear responsibilities and rigorous training, you signal to regulators that your firm takes its protective mission seriously. To help your team stay ahead of evolving social engineering threats, we recommend implementing structured Cybersecurity Awareness Training that provides measurable results and the documentation necessary for your compliance records.

Designating Your Qualified Individual

A central requirement of the rule is the designation of a “Qualified Individual” (QI). This person is tasked with the implementation and oversight of your entire information security program. It’s a common misconception that the QI must be a specialized IT professional or hold a computer science degree. The individual simply needs the capacity to manage the program and the authority to report on its status. For many smaller firms, the owner serves in this capacity. The QI’s responsibilities include providing an annual written report to the board of directors or senior management, detailing the overall status of the security program and any material matters related to it.

Service Provider Management

Your legal obligations extend to the third-party service providers you use. Whether it’s your tax preparation software or your secure cloud backup provider, you must ensure these partners maintain safeguards that meet GLBA standards. This oversight process involves vetting vendors before signing a contract and requiring them, by contract, to implement and maintain those safeguards. Don’t hesitate to ask for SOC 2 Type II reports or other independent security certifications. This documentation proves that your vendors are as committed to data protection as you are, creating a defensible chain of custody for your clients’ most sensitive information.

Professional Compliance Management: Protecting Your Firm’s Legacy

Viewing glba compliance for tax preparers solely as a regulatory hurdle ignores its significant value as a strategic business asset. In an era where high-net-worth clients are increasingly aware of digital threats, your commitment to security serves as a powerful differentiator. By aligning your practice with FTC mandates and IRS Publication 4557 standards, you position your firm as a high-integrity partner capable of protecting sensitive financial legacies. This proactive stance transforms compliance from a mandatory expense into a foundational element of your brand’s reputation.

A professional Written Information Security Plan (WISP) acts as a legal shield during federal inquiries. If the IRS or FTC ever questions your data handling practices, a documented, assessment-based plan proves that you’ve exercised due diligence. Relying on a “template-only” approach is a dangerous gamble that often fails during a rigorous audit. Generic plans rarely reflect the specific technical controls or administrative procedures of your office, leaving you vulnerable to claims of negligence. A truly defensible program must be as unique as the practice it protects.

The Cost of Non-Compliance vs. The Investment in Security

The financial consequences of a data breach or a failed audit can be devastating. Beyond the immediate $100,000 fine per violation, the long-term cost includes reputational damage and the potential loss of your PTIN. Professional risk assessments prevent the common pitfall of “over-spending” on generic technology that doesn’t actually address your firm’s specific vulnerabilities. By identifying exactly where your risks lie, you can allocate resources toward the precise safeguards that provide the highest level of protection. This targeted investment offers invaluable peace of mind, especially during the high-stress environment of tax season.

How Apex Tech 4 Tax Pros Simplifies GLBA Compliance

We understand that tax professionals are already managing complex federal requirements for their clients. Our mission is to handle the technical and regulatory heavy lifting so you can focus on your practice. We move beyond free templates to provide a customized WISP that accurately reflects your operations and meets 2026 standards. Our expert-led risk assessments are designed to identify hidden gaps in your infrastructure, ensuring that your security program is both comprehensive and compliant. Don’t leave your firm’s future to chance. Secure your firm today with a customized WISP and professional risk assessment.

Securing Your Practice and Your Clients’ Future

Achieving glba compliance for tax preparers isn’t just about avoiding a $100,000 fine; it’s about fortifying the trust your clients place in you every day. We’ve established that a defensible security program requires moving beyond generic templates toward a customized, risk-based framework. By implementing mandatory technical controls like multi-factor authentication and maintaining a living Written Information Security Plan, you transform a regulatory burden into a resilient shield for your firm’s legacy. This proactive approach ensures that your practice remains audit-ready and resilient against the sophisticated threats of 2026.

You don’t have to navigate these complex federal mandates alone. With decades of experience in technical compliance and a specialized focus on tax and accounting professionals, we help you implement security frameworks that are fully IRS and FTC compliant. Protecting sensitive data is a mission that requires both technical precision and a deep understanding of your professional environment. Get Your Free WISP Template or Schedule a Professional Risk Assessment to ensure your practice is prepared for the high-stakes demands of modern data protection. You’ve spent years building your reputation; let’s work together to keep it secure.

Frequently Asked Questions

Who is considered a “financial institution” under the GLBA?

Tax preparers, accountants, and even solo practitioners are considered financial institutions under the GLBA. The FTC defines these as businesses significantly engaged in financial activities, which includes providing tax preparation services to the public. This classification applies regardless of whether the firm is a large corporation or a home-based business.

Do solo tax preparers really need a Written Information Security Plan (WISP)?

Yes, every tax preparer must maintain a Written Information Security Plan regardless of firm size. While firms with fewer than 5,000 consumers are exempt from specific documentation like written risk assessments, they’re still legally required to implement and maintain a comprehensive information security program. A well-structured plan serves as your primary defense during an audit.

What are the penalties for GLBA non-compliance in 2026?

Financial institutions can face fines of up to $100,000 for each violation of the Safeguards Rule. Individual officers and directors can be fined up to $10,000 per violation and may face up to five years of imprisonment for severe negligence. These penalties reflect the high stakes of protecting sensitive financial data.

What is a “Qualified Individual” and do I need to hire someone new for this role?

A Qualified Individual is a designated person responsible for managing and overseeing your security program. You don’t necessarily need to hire a new employee; the role can be filled by an existing staff member or even the firm owner. The primary requirement is that they have the authority and capacity to implement the plan effectively.

How often does a tax firm need to update its risk assessment?

You should update your risk assessment periodically or whenever there’s a significant change to your firm’s technical environment. For larger firms, the FTC specifically mandates annual penetration testing and semi-annual vulnerability assessments. Smaller firms should still review their risks annually to account for new cyber threats and software updates.

Is multi-factor authentication (MFA) legally required for all tax software?

Multi-factor authentication (MFA) is a mandatory technical safeguard for anyone accessing systems that contain customer information. This requirement is a central component of glba compliance for tax preparers and applies to all software and cloud platforms where sensitive taxpayer data is stored. It’s the most effective barrier against credential theft.

Does a WISP cover the requirements for IRS Publication 4557?

A robust WISP is designed to meet both FTC Safeguards and the security plan requirements outlined in IRS Publication 4557. Achieving glba compliance for tax preparers through a comprehensive plan provides a unified defense that satisfies both agencies’ mandates. It ensures you meet mandatory federal security standards across all governing bodies.

What should I do if my tax firm experiences a data breach under the new FTC rules?

If a breach affects 500 or more consumers, you must notify the FTC within 30 days of discovery. This requirement became effective April 24, 2024, and applies to non-bank financial institutions. You must have a clear process for identifying and reporting these incidents to remain in legal standing with federal regulators.