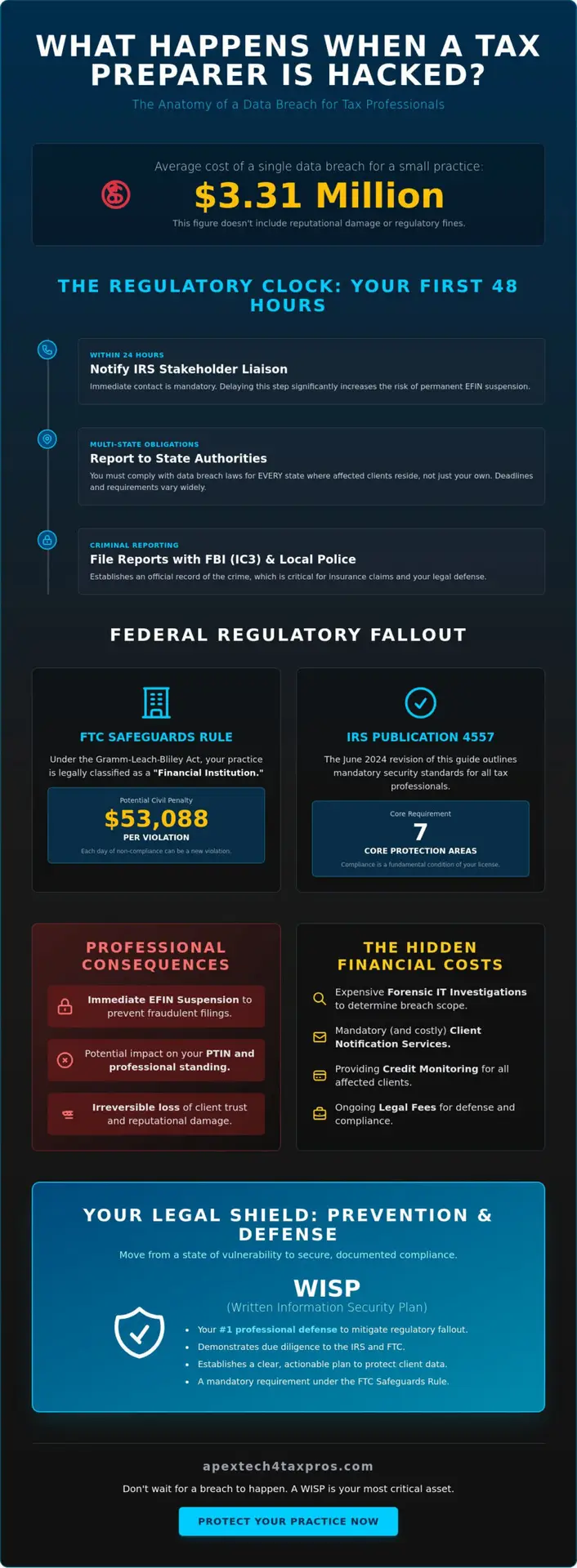

A single compromised password can trigger a cascade of federal enforcement actions that most firms aren’t prepared to handle. For a small practice, the average cost of a data breach has reached $3.31 million, but the professional damage often starts with a single, harrowing question: what happens if a tax preparer gets hacked? Under the Gramm-Leach-Bliley Act, your firm is classified as a financial institution, meaning the FTC can impose civil penalties of up to $53,088 per violation for non-compliance with the Safeguards Rule. Each day you remain out of compliance can be treated as a separate violation, making the financial stakes as high as the reputational ones.

You likely feel a deep sense of responsibility for your clients’ sensitive information, and the anxiety surrounding potential IRS EFIN suspensions or multi-state notification laws is entirely justified. This guide is designed to replace that uncertainty with a pragmatic plan of action. You’ll learn the mandatory reporting steps required by the June 2024 revision of IRS Publication 4557, the severity of current federal penalties, and the specific role of a Written Information Security Plan in protecting your practice from total fallout. We’ll move from a state of vulnerability to a state of secure, documented compliance.

Key Takeaways

- Identify the critical 24-hour reporting window to the IRS Stakeholder Liaison and your mandatory obligations to state revenue departments following a breach.

- Understand the specific regulatory requirements of the FTC Safeguards Rule and the seven core protection areas outlined in the June 2024 revision of IRS Publication 4557.

- Learn exactly what happens if a tax preparer gets hacked regarding the immediate suspension of your EFIN and the potential impact on your PTIN and professional standing.

- Recognize the hidden financial burdens of a data incident, including the significant costs of forensic IT investigations and mandatory client notification services.

- Establish a professional defense by implementing a customized Written Information Security Plan (WISP) to mitigate regulatory fallout and protect your practice’s future.

Immediate Mandatory Reporting: The First 48 Hours After a Breach

The discovery of a data breach triggers an immediate, high-stakes regulatory clock. Within the first 24 to 48 hours, your priority shifts from technical troubleshooting to mandatory legal reporting. Failing to act within these tight windows doesn’t just complicate your recovery; it can lead to the permanent loss of your professional credentials. When considering what happens if a tax preparer gets hacked, the most immediate consequence is the activation of federal and state oversight protocols that require precise, documented transparency.

Notifying the IRS Stakeholder Liaison

The IRS requires notification within 24 hours of discovering a breach. You must contact your local IRS Stakeholder Liaison immediately. These professionals serve as the primary link between the tax community and the IRS. To find your specific liaison, you should visit the official IRS website and search by your state. During this initial contact, the IRS will request specific data points, including your Electronic Filing Identification Number (EFIN), the approximate number of clients affected, and the date the compromise occurred. Delaying this notification is a significant risk. The IRS has the authority to suspend your EFIN immediately to prevent fraudulent returns from being filed under your credentials, and a failure to report the incident promptly makes that suspension much more likely to become permanent.

State-Level Data Breach Notification Laws

Reporting requirements extend far beyond federal authorities. You are legally obligated to follow the Data breach notification laws of every state where your affected clients reside. This is a common point of confusion for many practitioners. If you are based in Texas but have clients in California and New York, you must comply with the specific statutes and timelines of all three states. Some jurisdictions have notification windows as short as 30 days; others require immediate reports to the State Attorney General if a certain threshold of residents is impacted. Late notification can result in severe civil penalties and aggressive state-level audits from state departments of revenue.

Simultaneously, you must file a report with the FBI’s Internet Crime Complaint Center (IC3) and local law enforcement. This establishes an official record of the crime, which is essential for insurance claims and professional defense. Finally, contact your cyber insurance carrier. They’ll typically initiate a forensic investigation to determine the exact scope of the breach. This step is critical because you can’t accurately notify clients or regulators until a professional forensic team confirms exactly what data was accessed. Understanding what happens if a tax preparer gets hacked means recognizing that your response is no longer just a private business matter; it’s a matter of public and regulatory record.

Federal Regulatory Fallout: FTC Safeguards Rule and IRS Pub 4557

A data breach is far more than a technical failure; it is a regulatory event that triggers an immediate shift in how federal agencies view your practice. Once the initial reporting is complete, the focus of the IRS and the FTC moves toward your prior adherence to established security standards. Understanding what happens if a tax preparer gets hacked requires looking past the immediate technical recovery to the rigorous compliance audit that follows. Federal regulators do not view security as a secondary concern; they view it as a fundamental requirement of your professional license.

The FTC Safeguards Rule Enforcement

Under the Gramm-Leach-Bliley Act, tax preparers are legally classified as “financial institutions.” This classification subjects even the smallest solo practice to the full weight of the FTC Safeguards Rule. As of 2026, the FTC has the authority to levy civil penalties of up to $53,088 per violation. For the FTC, a violation isn’t just the breach itself; it’s the absence of the mandated safeguards that should have prevented it. This includes the requirement to designate a “qualified individual” to oversee your security program. If you cannot produce documentation showing who was responsible for your security and what specific risks they assessed, the financial fallout can escalate quickly.

IRS Publication 4557 Compliance Audits

The regulatory response to what happens if a tax preparer gets hacked is methodical and unforgiving. The IRS uses Publication 4557, specifically the June 2024 revision, as the definitive checklist for “reasonable security.” When a breach occurs, an IRS agent or Stakeholder Liaison will likely ask to see your Written Information Security Plan (WISP). This is not a request for a generic template; they are looking for a living document that outlines how you protect data across seven specific areas, including employee management and hardware security. Failing to provide a customized WISP is often treated as a “willful neglect” of federal standards, which can lead to the immediate suspension of your EFIN and PTIN.

The “reasonable security” standard is a common trap for practitioners who believe that basic antivirus software is sufficient protection. In a post-breach audit, “doing your best” is not a valid legal defense. Regulators look for evidence of continuous monitoring, encrypted backups, and multi-factor authentication. If these controls were absent, the breach is viewed as a predictable result of negligence. A proactive Risk Assessment can identify these documentation gaps before a breach forces a federal inquiry. Compliance with Pub 4557 doesn’t just prevent breaches; it serves as your primary evidence that you took every required step to protect your clients, which can significantly mitigate the severity of federal penalties.

Professional Consequences: EFIN Suspension and Loss of Practice

The regulatory fines discussed previously are significant, but the true existential threat to your practice lies in the loss of your professional credentials. When analyzing what happens if a tax preparer gets hacked, the most devastating blow is often the immediate suspension of your Electronic Filing Identification Number (EFIN). The IRS views a data breach as a compromise of the entire tax ecosystem. If your credentials have been used to facilitate fraudulent filings, the agency will move to protect the system by revoking your ability to transmit returns. This isn’t a mere administrative delay; it’s a complete cessation of your primary revenue stream.

EFIN Suspension and Business Continuity

The suspension of an EFIN effectively creates a “blacklist” scenario. Once your EFIN is flagged, you cannot e-file for any client, regardless of whether their specific data was compromised. During the peak of tax season, this freeze is often a death knell for small firms. Appealing an EFIN suspension is a bureaucratic process that requires demonstrating that you have fully remediated your security vulnerabilities. Without a comprehensive response that aligns with IRS Publication 4557, this process can drag on for months. Many firms simply don’t have the cash reserves to survive a mid-season filing freeze, leading to a permanent loss of their client base to competitors who can still guarantee timely filings.

Professional Licensing Board Actions

Your standing with the IRS isn’t the only concern. A data breach often triggers referrals to the Office of Professional Responsibility (OPR) for potential violations of Circular 230. This regulation governs the conduct of practitioners before the IRS, and a failure to protect client data can be interpreted as a failure to exercise due diligence. For CPAs and Enrolled Agents, this can lead to “unprofessional conduct” charges from State Boards of Accountancy. The potential consequences include:

- Public Censure: A permanent, searchable record of your professional failure that clients can easily find.

- Monetary Penalties: Fines that are levied against you personally, rather than just the business entity.

- License Revocation: The total loss of your right to practice as a CPA or Enrolled Agent.

When considering what happens if a tax preparer gets hacked, the risk to your PTIN (Preparer Tax Identification Number) is just as severe as the risk to your EFIN. If your PTIN is suspended, you are legally prohibited from signing any tax return for compensation. This effectively ends your career in tax preparation until the suspension is lifted, a process that can take years of legal maneuvering and high-priced counsel. Protecting your license requires more than just intent; it requires documented proof of Cybersecurity Awareness Training and other mandatory safeguards. The professional standing you spent decades building can be dismantled in a single afternoon if your firm’s security posture is found wanting.

The Hidden Financial Costs of a Tax Data Breach

The regulatory fines levied by the FTC and IRS represent only the visible portion of a much larger financial burden. While a $50,000 penalty is significant, it is frequently dwarfed by the operational and legal expenses required to stabilize a firm after an incident. When analyzing what happens if a tax preparer gets hacked, practitioners must account for the immediate drain on cash reserves and the long-term erosion of their firm’s valuation. These costs are not theoretical; they are the direct result of mandatory remediation protocols and the modern litigation environment.

Forensic Audit and Remediation

You cannot simply wipe a hard drive and resume operations after a breach. Regulatory bodies and insurance carriers require a certified forensic investigation to determine the exact point of entry and the specific records compromised. These specialized IT firms charge significant fees to provide the “clean bill of health” necessary to restore your EFIN. Based on 2026 industry data, the average cost of a data breach for businesses with fewer than 500 employees has reached $3.31 million. In the financial services sector specifically, which includes tax practices, the average total cost of an incident is approximately $5.56 million. These figures include the cost of identifying the vulnerability, closing the security gap, and certifying that no dormant malware remains in your infrastructure.

Civil Litigation and Client Trust

Class-action lawsuits are no longer reserved for multinational corporations. Small accounting and tax firms are increasingly targeted by litigation following a data exposure. If your firm lacks a Written Information Security Plan (WISP), plaintiff attorneys will use that absence as primary evidence of professional negligence. They will argue that the breach was not an unavoidable accident but a predictable result of failing to meet federal “reasonable security” standards. Beyond the courtroom, you face the “Reputation Tax.” This is the quantifiable loss of revenue as clients migrate to competitors who can demonstrate a more robust security posture. Retaining a client after notifying them that their Social Security number and financial history are in the hands of criminals is a marketing challenge that many firms fail to overcome.

The financial fallout is often dictated by your level of preparation before the attack. A tested incident response plan can reduce the total cost of a breach by an average of $232,007, providing a clear financial incentive for proactive compliance. To understand where your firm stands before a crisis occurs, you should conduct a professional Risk Assessment to identify and close these expensive security gaps. Investing in prevention is the only way to avoid the cascading costs of forensic audits, legal defense, and the permanent loss of client trust.

The WISP as Your Legal Shield: Preventing the Worst Case

While the previous sections detailed the wreckage of a data breach, the goal of every practitioner should be to establish a “Safe Harbor” defense. A Written Information Security Plan (WISP) is not merely an administrative hurdle; it is your primary legal shield. When regulators investigate what happens if a tax preparer gets hacked, they look for evidence that the firm met the “reasonable security” standard before the incident occurred. A comprehensive WISP provides this evidence, potentially transforming a catastrophic failure into a managed event with significantly reduced penalties and a faster path to EFIN restoration.

Building an IRS-Compliant WISP

To satisfy the FTC Safeguards Rule, a WISP must address specific technical and administrative controls, including encryption, multi-factor authentication, and strict service provider oversight. However, a static document downloaded from the internet is rarely sufficient to protect a practice. Regulators require the plan to be a “living document” that undergoes annual updates and reflects the firm’s actual digital environment. Apex Tech 4 Tax Pros specializes in developing a Customized Written Information Security Plan (WISP) that aligns with your specific operational needs rather than relying on generic, non-compliant placeholders. This level of customization is what distinguishes a professional defense from a documentation liability.

Proactive Risk Assessments and Training

Technology alone cannot secure a tax practice because 88% of small business data breaches involve a human element, often through ransomware or sophisticated phishing campaigns. This reality makes Cybersecurity Awareness Training an essential component of your firm’s security posture. By educating your staff on the latest social engineering tactics, you close the most common point of entry for cybercriminals. Additionally, regular Risk Assessments allow you to identify hardware and software vulnerabilities before they can be exploited. Having a tested incident response plan as part of these assessments can reduce the total cost of a breach by an average of $232,007, providing a clear financial incentive for proactive compliance.

Adopting a “Security-First” philosophy allows you to rebuild client trust by demonstrating a commitment to data protection that exceeds minimum federal requirements. It changes the conversation from a fear of what happens if a tax preparer gets hacked to a position of professional strength and regulatory resilience. Positioning your firm as a multidisciplinary protector of both financial and personal data is the most effective way to secure your legacy in an increasingly hostile digital landscape. Protect your practice and your clients by taking action today. Schedule a professional risk assessment with Apex Tech 4 Tax Pros today.

Securing Your Professional Legacy and Regulatory Compliance

The professional landscape for tax practitioners has evolved into a high-stakes environment where technical security is now inseparable from legal standing. Understanding what happens if a tax preparer gets hacked reveals a rigorous path of immediate IRS reporting, potential EFIN suspension, and devastating civil litigation costs. These outcomes aren’t inevitable for firms that treat data protection as a core professional duty. By moving beyond generic templates and implementing a living, documented security strategy, you transform your practice from a state of vulnerability into one of resilient compliance.

Our team specializes exclusively in the tax and accounting industry, providing the specialized expertise required to navigate the June 2024 revision of IRS Publication 4557 and the amended FTC Safeguards Rule. We ensure your firm is protected by a strategy engineered for your specific operational needs. Protect Your Practice: Get Your Customized WISP Now.

You’ve spent years building your reputation and your client base. Taking these proactive steps today ensures that your practice remains a trusted, secure pillar for your clients for decades to come. We’re ready to help you secure that future.

Frequently Asked Questions

Is it illegal for a tax preparer not to have a WISP?

It is a violation of federal law to operate without a Written Information Security Plan (WISP). Under the Gramm-Leach-Bliley Act and the FTC Safeguards Rule, all tax preparers are classified as financial institutions. This classification mandates a documented security program that protects client data. Failing to maintain a current WISP can lead to significant civil penalties and the immediate suspension of your professional filing credentials by the IRS.

Can I be sued by my clients if my tax practice is hacked?

Clients have the legal right to pursue civil litigation if their sensitive data is exposed due to your firm’s negligence. In many class-action cases, the absence of a required WISP is used as evidence that the practitioner failed to meet the “reasonable security” standard. These lawsuits often seek damages for identity theft protection services, financial losses, and emotional distress, which can quickly exceed a firm’s operational capital.

What is the first thing I should do if I suspect a data breach?

Your first priority is to contact your local IRS Stakeholder Liaison within 24 hours of discovery. This immediate step allows the IRS to monitor for fraudulent returns filed under your EFIN. Simultaneously, you should engage your cyber insurance carrier to initiate a professional forensic investigation. Prompt reporting is essential to mitigating the fallout and understanding what happens if a tax preparer gets hacked in terms of regulatory leniency.

Will the IRS shut down my EFIN if I get hacked?

The IRS will frequently suspend an Electronic Filing Identification Number (EFIN) immediately following a breach to protect the integrity of the tax system. This suspension remains in place until you can demonstrate that your systems are secure and that you’ve met all reporting requirements. Regaining your trusted provider status requires a thorough remediation process and documented proof that your security protocols have been fully updated.

Does my professional liability insurance cover data breaches?

Standard professional liability or “errors and omissions” insurance typically doesn’t cover the costs associated with a data breach. Most practitioners require a specific cyber liability policy or a dedicated rider to cover forensic audits, client notifications, and legal defense fees. It’s critical to review your policy details annually, as many carriers now require proof of a WISP as a condition for maintaining active coverage.

How much are the fines for FTC Safeguards Rule non-compliance?

The FTC can levy civil penalties of up to $53,088 per violation for non-compliance with the Safeguards Rule. It’s important to understand that the FTC may consider each day of non-compliance or each individual record compromised as a separate violation. These fines are adjusted annually for inflation and represent a significant financial risk for firms that fail to document their security measures as required by federal law.

Do I have to notify every client, even if their data wasn’t stolen?

Notification requirements are governed by the specific data breach laws of the state where the client resides. While some states only require notification if there’s a reasonable likelihood of harm, most practitioners notify their entire client base as a transparency measure. You should rely on the findings of a professional forensic audit to determine exactly which records were accessed before sending out official, legally mandated notifications to your clients.

How often should a tax firm perform a cybersecurity risk assessment?

You should perform a comprehensive cybersecurity risk assessment at least annually or whenever there’s a significant change to your firm’s technology or operations. The IRS and FTC view these assessments as essential for maintaining a “living” security program. Regular testing ensures that your safeguards remain effective against evolving threats and provides the necessary documentation to prove compliance if your practice ever faces a regulatory audit or a breach investigation.